Well, the time has come to update the Freedom Fund once again as we start another month. The Freedom Fund is my portfolio, and I think it’s aptly named. My portfolio is my way to freedom; freedom from a job I don’t desire to purchase goods I don’t need to impress neighbors I don’t care about. This journey is all about freedom and flexibility. One day, the dividend income this portfolio generates will fully cover my expenses and my time will be completely my own. What could you possibly want to own more than your time?

I’m extremely fortunate that I’m able to post these updates every single month, which shows the power of monthly contributions to investments because of the high savings rate I maintain. It shows how a relatively large sum of money can be built through the power of time, patience and perseverance.

It’s important to keep in mind that while updating the overall value of my portfolio is important for historical reference and keeping track of total return, as well as giving context to the dividend income I earn, my main focus is on the rising dividend income stream the Fund provides.

But I’m living up to the message I preach: Choose time over money. Choose freedom over slavery. Choose passion over work. Choose simplicity over complexity. I’ve freed up time by simplifying my life, which will allow me to focus on my passions.

September was off to a roaring start even before these changes were cemented, but I definitely finished strong. All in all, I couldn’t be more pleased to see my cash flow get this temporary increase exactly at the same time that volatility across the broader stock market has also increased. Time in the market matters more than timing the market for the long-term investor, but I’ll tell you that I wouldn’t mind being able to somehow take advantage of both whenever possible.

Now, I don’t sell stocks very often. I’ve published just 10 articles discussing stock sales on this blog since early 2011 (against more than 120 “Recent Buy” articles), and that’s because I’m a buy-and-hold long-term investor. Selling off pieces of great companies limits the effects of compounding and your ability to build a growing snowball. However, I did record a couple sales this month. I first eliminated my position in BHP Billiton PLC (BBL) completely by selling all 115 shares at $33.28. I then significantly reduced my position inNational Oilwell Varco, Inc. (NOV) by selling off 65 shares at $38.62.

I didn’t sell stock in these companies because I’m any less enthusiastic about their long-term prospects. It was simply a tax move. I used a tax-loss harvesting strategy to reduce the more than $3,000 in capital gains I registered this year after Medtronic PLC (MDT) acquired Covidien PLC and relisted its stock, and Lorillard Inc. was acquired by Reynolds American, Inc. (RAI). I’m now down to essentially $0 in gains this year, which should reduce my tax bill by more than $450. I’ll be buying back into BBL and NOV as soon as the 30 days relating to the wash rule is up.

So the sale of stock in BBL and NOV provided me with even more firepower (more than $6,000) for my BB gun than usual, which, when combined with particularly strong near-term cash flow, meant I was flush with capital. And as I’ve said over and over again, I prefer cash flow (especially growing, passive cash flow in the form of increasing dividends) to cash, which is exactly why I went on a shopping spree so as to convert the latter into the former.

Now, I started the month off with adding to my position in Omega Healthcare Investors Inc. (OHI). I really, really like this business and its business model. Love the valuation, the yield, the quality, and the future prospects. Toward the middle of the month I picked up another 45 shares at $33.12 per share. Not sure I’ll add any more, as I’m pretty comfortable now with 150 shares.

A similar real estate investment trust, HCP, Inc. (HCP) has long been on my radar, but I’ve felt (and still feel) like Omega Healthcare is the better business, overall. However, my position in OHI is now quite large and I like the diversification that HCP offers (operating across senior housing, post-acute/skilled nursing, life science, medical office and hospital). Moreover, the valuation and yield are also both compelling (like with OHI). I initiated a stake in HCP with 30 shares at $38.24 just before the Fed announced that interest rates wouldn’t change over the near term. HCP’s stock zoomed up, but then fell back down with weakness across the broader market. Perfect! Just the opportunity I needed to double my position at a cheaper price – I added another 30 shares at $36.97. This stock yields over 6% with 30 consecutive years of dividend raises.

I also added to my positions in a couple energy supermajors for the first time in a long time. I haven’t been particularly interested in a lot of energy plays, especially supermajors, lately due to a combination of my overexposure to the Energy sector as well as concerns over some stocks holding up a bit better than I had expected them to.

But I’ve been buying around these stocks, slowly reducing their weightings. And Royal Dutch Shell PLC (RDS.B) and BP PLC (BP) have been hammered over the last year, even though they weren’t that expensive from the get-go due to company-specific issues. Both now have sky-high yields (supported by plenty of cash) and the valuations are extremely compelling here, respectively speaking. Moreover, I had a little room in the portfolio for both, especially RDS.B. So I picked up 30 shares of BP at $30.76 per share and 20 shares of RDS.B at $50.74 per share.

Staying a little more active in the energy patch than I had planned on (or really wanted to) due to extreme volatility, I also added to my stake in Kinder Morgan Inc. (KMI). The stock is down almost 15% over just the last month and almost 35% YTD. It now yields over 7% even though a lot of the company’s revenue is fee-based, with limited exposure to commodity pricing. I didn’t plan on ever buying any more stock in Kinder Morgan due to my position size, but I just couldn’t pass it up here. Didn’t go too crazy, however, adding just 25 shares at $27.95.

ONEOK, Inc. (OKE), another high-quality midstream play, has also been absolutely hammered – it, too, is down ~35% YTD. This is another stock I wasn’t particularly interested in buying more of due to my general exposure to energy and more specific exposure to midstream pipeline companies, but the valuation was screaming at me. I grabbed more OKE twice this month – 15 shares at $34.39 and 20 shares at $30.84.

I then initiated a position in Colgate-Palmolive Company (CL) at $62.38 per share. Picked up a hefty 50 shares here. Admittedly, I paid a little more for this stock than I would have liked. But it’s a stock I’ve long wanted to add to the collection, and I don’t think the valuation is completely outrageous or anything. It’s a little pricey, but it also depends on what future dividend growth turns out to be. The company is about as high quality as it gets, and I love the brand power here. I paid up for quality here.

I was also quite busy in the Industrials space this month, as I happen to think that there are a lot of high-quality companies in this sector trading hands at extremely compelling valuations for long-term investors.

I added to my position in United Technologies Corporation (UTX) twice – picking up 15 shares at $92.61 and another 10 shares at $87.91. I also added to my stake in Caterpillar Inc. (CAT) after the stock fell off a cliff, down substantially after announcing layoffs amid softness in key end markets. I purchased 10 shares at $65.79. This isn’t a company that I see myself investing heavily in, but I couldn’t pass it up here. If it drops substantially more, I might add another handful of shares, but that would probably be it. I also added to my stake in Emerson Electric Co. (EMR) at what seems to be a ridiculous price – grabbing 25 more shares at $44.28. I’ll probably just hold pat now with 105 shares in Emerson. Yielding well over 4% with a P/E ratio of just over 12, Emerson – with its 58 consecutive years of dividend increases – is a no-brainer here.

But I didn’t just add to existing stakes in high-quality Industrials.

After many years of watching this stock relentlessly rise, 3M Co. (MMM) finally took a short breather and I jumped on it. I initiated a position in MMM with 10 shares at $137.41. 3M is an amazing company that has exposure to just about every industry in the world. Love the thought of owning a small slice of more than 100,000 patents. Another great company that I’ve watched for some time, Fastenal Company (FAST), has also become quite reasonably priced lately after falling more than 20% YTD. No debt, yield over 3%, double-digit long-term dividend growth, and operating in a great niche. I bought 50 shares at $37.50. This is another new position for the Fund.

I also went hunting in the Financials sector.

I initiated a stake in ACE Limited (ACE), a global insurer that’s extremely high quality by itself, but that will likely be even higher quality after the acquisition of Chubb Corp. (CB) (assuming it goes through). I think the valuation is fairly attractive here considering the prospects and track record – they’ve increased their dividend for the past 23 consecutive years with a 10-year dividend growth rate of 12.3%. Flies under the radar, but probably shouldn’t. My stake in ACE was started off with 15 shares at $101.80 per share.

Canadian banks have also been incredibly weak lately. Bank of Nova Scotia (BNS) is down more than 20% on the year, bringing the valuation down to a very attractive level and the yield up to over 5%. Fundamentals remain sound, however, and I had a little room in the portfolio. Added 20 shares at $43.06. I also added to my position in Toronto-Dominion Bank (TD) for the same reasons. Was fortunate enough to be able to buy 24 shares at $38.42.

One industry I’m not a huge fan of is retailing. Nonetheless, there are a few great retailers out there with outstanding dividend growth track records, strong competitive advantages, and excellent fundamentals (relatively speaking; big margins are hard to come by here). Wal-Mart Stores, Inc. (WMT) is one such retailer. More than 40 consecutive years of dividend growth, though recent dividend raises have left something to be desired. Still, a low payout ratio and plenty of free cash flow gives me hope that they’ll be back on the horse soon. The valuation is also very compelling here however you look at it, especially with a yield that’s more than 70 basis points higher than the five-year average. I added to my stake in the world’s largest retailer by purchasing 10 shares at $63.76.

Anyone following recent news will know that biotechnology stocks were hammered after Hillary Clinton tweeted about drug pricing. This kind of stuff makes me laugh. I ignore the noise and keep my eye on the long term. Although this came right around the time my cash was almost exhausted for the month, I did have a few BBs left in the gun. Adding just 5 shares to my Gilead Sciences, Inc. (GILD) stake at $95.81, it was the perfect spot for me. I view GILD as a speculative play due to the business model and newly issued dividend, and this small transaction was right-sized for my cash flow and willingness to invest more.

Finally, I initiated a position with 10 shares at $104.99 in Diageo PLC (DEO). This is another stock that has been on my watch list for what seems like forever. I’ve long wanted that exposure to the world’s largest spirits producer, with leading brands ranging from Smirnoff to Johnnie Walker to Baileys. Although I have some indirect exposure to alcoholic beverages through my position in Altria Group Inc. (MO) and its 27% ownership stake in SABMiller PLC (SBMRY), I wanted to own a stake myself in a great company in this space. And I don’t think it gets any better than DEO with their unrivaled scale and collection of brands. Moreover, while major beer producers become somewhat marginalized by craft brewers, the business of large-scale spirits seems to remain robust.

Whew! What a month!

I’ve never experienced anything like it, and it’s unlikely I’ll ever experience anything like that ever again. But it was incredible while it lasted. I felt like I was running an insurance company with a really tiny float that was sending cash flow my way to buy stocks. It must be what Warren Buffett feels like for, oh, about 1/10 of 1 second.

The sales reduced my annual dividend income by $401.80, though I plan on building my stakes in BBL and NOV back up in October. Both positions will probably be a bit smaller when it’s all said and done, but that’s only because those positions were bigger than I ever planned on them being.

However, the purchases added $1,089.16 to my annual dividend income. So the net addition to my annual dividend income (after factoring out the sales) was $687.36. Just absolutely incredible. That’d be a niceannual addition, so the fact that I was able to do this in just one month just really speaks to how fortunate I am. It’s been a really, really fun and busy summer, with both June and September both being absolute bonanzas for stock purchases.

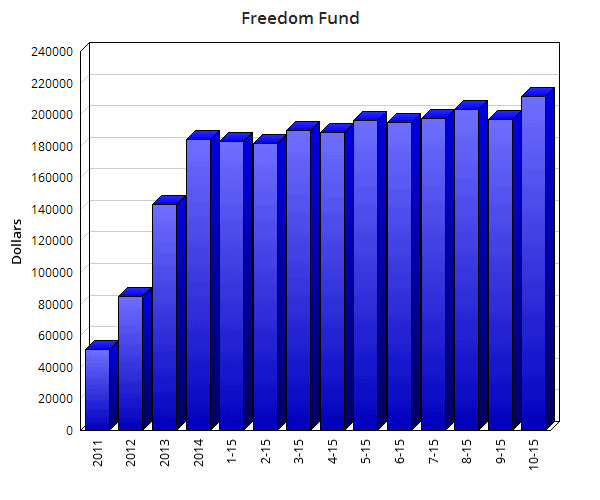

The current market value of the Freedom Fund stands at $211,444.20, which is a 7.4% increase since last month’s published value of $196,826.45.

The Fund continues to prosper and hold up really well. Heavy exposure to some big names in the energy patch adds a little volatility, but, overall, the swings on a day-to-day basis really aren’t that bad. Moreover, I don’t mind volatility at all. Quite the contrary, I view short-term volatility as a long-term opportunity, hence the activity you see above.

This past month (and, really, the entire summer) has resulted in far more activity than my historical norm. Up until the summer, I’ve averaged a rate of about $2,000 in monthly fresh capital. So this is way above my long-term average. And it doesn’t look set to last, unfortunately. As I’ve noted a few times, my long-term cash flow is going to be reduced somewhat substantially due to the changes I’ve made to the blog. As such, I’m trying to make up for some of that via dividend income. Moving forward, I’ll be a bit more aggressive in terms of yield than I’ve been over the last year or so so as to increase my current dividend income as much as possible (though, not sacrificing quality in the process), which will, perhaps, move my overall time line up a bit. We’ll see about that.

Either way, thank you all for your continued support. I can only hope that this post adds some value for you. You can see exactly where I’m putting capital to work with recent volatility, and I think all of the above stocks offer something to like. I’m certainly glad to add these stocks to my collection, which I think boosts the quality, overall. But you’re looking at a nice mix of industries there, along with value and yield.

The Fund now has positions in 70 different companies. This is an increase since last month. I eliminated my position in BBL, but made that up with initiating stakes in six different companies. I can see the Fund one day having exposure to 80 or 90 companies, but, looking at my watch list, I don’t foresee extending past 100 companies.

These updates are mainly designed to show the increase or decrease in the value of the underlying equities I’m invested in, but the main purpose of investing in dividend growth stocks is to build a rising and sustainable stream of dividends over time. Thus, I don’t put too much emphasis on these monthly updates. I think it is a good idea, however, to keep track of the rising (or falling) value of one’s securities and be aware of where they are in terms of the marketplace and whether or not certain stocks are attractively priced. I find it a helpful exercise to update the values monthly. It gives me fresh perspective on which equities are performing well and which aren’t, and from there I can make educated decisions (based on further due diligence) on which stocks I’d like to add fresh capital to (while considering portfolio weight as well).

Full Disclosure: Long all aforementioned stocks except BBL, CB, and SBMRY.

Did you also have a busy September? Take advantage of all of the recent volatility?

Thanks for reading.

Photo Credit: BimXD/FreeDigitalPhotos.net

Edit: Added share count and price information for CL, ACE, and DEO.This article was written by Dividend Mantra. If you enjoyed this article, please subscribe to my feed [RSS]