3M Company (NYSE: MMM) is a diverse conglomerate that produces a broad array of products and materials for both consumers and businesses. -Seven Year Revenue Growth Rate: 4.46%

-Seven Year Revenue Growth Rate: 4.46%

-Seven Year EPS Growth Rate: 3.97%

-Seven Year Dividend Growth Rate: 9.85%

-Current Dividend Yield: 2.56%

-Balance Sheet Strength: Extremely Strong

-Seven Year EPS Growth Rate: 3.97%

-Seven Year Dividend Growth Rate: 9.85%

-Current Dividend Yield: 2.56%

-Balance Sheet Strength: Extremely Strong

Overview

3M Company (NYSE: MMM), once called the Minnesota Mining and Manufacturing Company, was founded in 1902. The company, now with 80,000 employees, produces products like Scotch tape, projector systems, Post-it notes, Tartan track, and Thinsulate. This is a conglomerate that produces products for many industries and for both personal and business use, and their manufacturing, research, and sales offices are all over the world.

Business Segments

The company is divided into five business segments:

Industrial Business

This segment provides adhesives, abrasives, filtration systems, fasteners, and specialty materials to a variety of industries. This is the largest segment, accounting for about 34% of sales.

Safety and Graphics Business

This segment provides display films, reflective materials, projection systems, and the like. This segment accounts for about 18% of sales.

Electronics and Energy

This segment provides products for electronics and energy businesses including films for LCD screens and splicing products for signal cables, and accounts for about 17% of sales. Nearly two-thirds of sales from this segment come from the Asia Pacific region.

Health Care Business

This segments provides several products in the areas of wound care, oral care, drug delivery systems, and more. This segment accounts for about 17% of sales. The bulk of sales come mainly come from the U.S. and Europe, as the products are more targeted towards developed countries.

Consumer and Office Business

This segment provides solutions for the home and office, and includes well-known products like Scotch tape. This segment accounts for about 14% of sales. The U.S. accounts for over half of sales from this segment.

This segment provides adhesives, abrasives, filtration systems, fasteners, and specialty materials to a variety of industries. This is the largest segment, accounting for about 34% of sales.

This segment provides display films, reflective materials, projection systems, and the like. This segment accounts for about 18% of sales.

This segment provides products for electronics and energy businesses including films for LCD screens and splicing products for signal cables, and accounts for about 17% of sales. Nearly two-thirds of sales from this segment come from the Asia Pacific region.

This segments provides several products in the areas of wound care, oral care, drug delivery systems, and more. This segment accounts for about 17% of sales. The bulk of sales come mainly come from the U.S. and Europe, as the products are more targeted towards developed countries.

This segment provides solutions for the home and office, and includes well-known products like Scotch tape. This segment accounts for about 14% of sales. The U.S. accounts for over half of sales from this segment.

Ratios

Price to Earnings: 21.21

Price to Free Cash Flow: 19.85

Price to Book: 7.3

Return on Equity: 31.72%

Price to Free Cash Flow: 19.85

Price to Book: 7.3

Return on Equity: 31.72%

Revenue

MMM revenue trend is very strong. Since 2012, revenue doesn’t increase at the same pace mainly because the company faces currency headwinds. The organic growth is present (4.9% in Q1 2015), but the negative impact of a strong dollar reduces sales significantly.

MMM revenue trend is very strong. Since 2012, revenue doesn’t increase at the same pace mainly because the company faces currency headwinds. The organic growth is present (4.9% in Q1 2015), but the negative impact of a strong dollar reduces sales significantly.

Earnings and Dividends

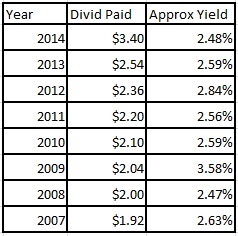

Approximate historical dividend yield at beginning of each year:

Approximate historical dividend yield at beginning of each year:

The company has been paying dividends each year for the past… 98 years. We can definitely talk about a strong dividend payer here. Most importantly, the dividend increase in 2014 and 2015 are stronger than its previous years. Nonetheless, the past 7 years shows an annualized dividend growth rate near double digits (9.85%). In other words, the company is nearly doubling its dividend payment every 7 years.

How Does 3M Company Spend Its Cash?

The company generates over 5 billion per year in free cash flow. The fact MMM is selling mostly consumable products makes its cash flow base stable and predictable. This enables the company to manage growth through R&D and acquisitions while returning a good amount of money to shareholders at the same time. In 2014, MMM used $1.5 billion for capital expenditures, $1.8 billion in R&D and $1 billion in acquisitions. At the same time, it has returned $7.9 billion to shareholders via a share repurchase program and dividend payments.

Investment Thesis

3M Company is definitely more diversified than a balanced mutual fund. It is present in various consumable product areas and the bulk of its sales comes from business-to-business transactions.

Roughly 50% of its products are consumable, which implies a very high rate of repeat business year after year. Product diversification is at the center of MMM business which offers continuous growth opportunities.

The company also allocates between $1 and $2 billion per year for acquisitions providing external growth on top of what is coming out of its own R&D department. MMM also benefits from top-of-the-line technology enabling to control costs like no other company. It can easily scale any production and each innovation means higher sales volume.

It is very hard to compete against MMM due to its size and investing power. Since the company keeps investing massively in R&D and buys other innovating companies, it ensures its sustainability over time.

Risks

When an investor buys MMM, he doesn’t expect to lose 40% of its value overnight. Product and geographic diversification enables the company to post predictable and stable numbers. However, these two advantages could also be linked to some other risks.

The fact MMM produces so many different products makes high digit growth difficult to generate. It is most likely to follow closely GDP growth instead of reaching high double digit figures.

MMM has increased its sales throughout the world in the past decade. This makes the company more at risk of currency headwinds.

As you can see, these are not the biggest concerns an investor could have while buying a stock. Overall, MMM shows a very strong profile.

Conclusion and Valuation

In my opinion, MMM should be part of most conservative (or core) dividend portfolios. While you shouldn’t expect incredible growth from this company, dividend payment increases will always be there each year. In order to verify if it’s the right time to buy MMM, we will look at the company 10 year PE history along with a Dividend Discount Model calculation.

As you can see, the strong dividend increase in the past 5 years hasn’t been ignored by the market. The P/E ratio has continuously increased over the past 3 years.

Full Disclosure: As of this writing, I have no position in MMM. It seems the company hasn’t been highly valued as right now. Let’s use the dividend discount model to see how much the company worth according to its dividend payment ability.

As you can see, the strong dividend increase in the past 5 years hasn’t been ignored by the market. The P/E ratio has continuously increased over the past 3 years.

Full Disclosure: As of this writing, I have no position in MMM. It seems the company hasn’t been highly valued as right now. Let’s use the dividend discount model to see how much the company worth according to its dividend payment ability.

Source: Dividend Toolkit

I’ve used a dividend growth rate of 10% for the first 10 years and reduced it to 7.5% afterward. Then, I used a discount rate of 9% since the company shows stellar numbers.

According to the DDM, the company trades at a discount of 15% or so with a fair value of $179. Strong dividend growth perspective justifies a higher P/E valuation at the moment.

Considering MMM product portfolio and the fact the company is making the bulk of its sales from consumable products in a business-to-business model, MMM seems fairly attractive at the current price. This is a “long-term-dividend-growth” stock for patient investors.

Disclaimer: I do not hold MMM in my portfolio.

This article was written by Dividend Monk. If you enjoyed this article, please subscribe to my feed [RSS]

This article was written by Dividend Monk. If you enjoyed this article, please subscribe to my feed [RSS]