For each stock analysis I perform on my blog or for my portfolios, I always include a section about valuation. To be honest, the valuation part of my analysis is not my favorite… and not the most important either in my opinion. I prefer working on my investment thesis and assessing potential risks than shaking my crystal ball and give a dollar value on the shares. Is it because I’m bad at giving valuation? Not really. The problem is that I’m well aware that regardless the method I use, there are severe limitations that could make two investors using the same model, but getting completely different results. Today I will take a look at the dividend discount model (DDM) limitations and how I deal with them.

How the Dividend Discount Model Works

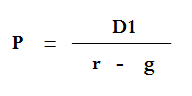

The reason I like using the DDM for my work is because the formula is simple and effective. The purpose of this model is giving a value for future dividend payments. It’s basically giving you the value of your “money making machine” based on how much it should pay you back in the future. The model has been built around the following formula:

P is the price of the stock, D1 is next year expected dividend, R is the rate of return (discount rate) and G is the dividend growth rate. Therefore, in order to complete the formula, you “simply” have to determine the discount rate and future dividend growth rate as the payable dividend is already known.

How can you make mistakes with such as simple formula? Unfortunately, nothing is simple in finance and while the DDM sounds simple, it comes with several shortcomings.

Dividend Discount Model Flaws

Regardless of the method you are using, the first flaw of all calculation models will be the same: the model is as good as its input. You can put any kind of numbers you want and results may vary. This is why it is so important to understand specific flaws for each model you use. Here’s the list for the DDM:

Constant dividend growth rate

Based on the original formula (also called the Gordon Growth Model), calculations are based on a constant dividend growth through time. This assumption is completely wrong and likely never going to happen in real life. For the rest of this article, I will use a well-known Dividend King: 3M Co (MMM). Here’s MMM dividend growth rate for the past 30 years:

Source: data from Ycharts

While MMM has increased its payout for 58 consecutive years, you can see that its dividend growth rate has greatly fluctuated overtime.

The Fix:

By digging into the company’s dividend growth rate history, you can get a better idea of its average. After looking at how management grew its payouts, you can also look at how revenues and earnings are growing recently. To improve your accuracy for the dividend growth rate, you can also use a double-stage DDM. This will allow you to select a first dividend growth rate for a specific period and a terminal growth rate for long term payouts.

Which Dividend Growth Rate?

Then again, we hit another difficult value to determine. Should you use the last year previous growth rate that is very close to the current company’s situation? Or should you give it some thought and consider a larger growth history?

The Fix:

If you use the double stage DDM, the first number should be close to what the company has been going through over the past 5 years and the terminal rate should reflect more the overall history of the company’s growth rate. This is not a simple task, but let’s takes a look at how MMM grew its dividend:

- 5 years: 14.77% annualized return

- 10 years: 9.367% annualized return

- 20 years: 7.73% annualized return

- 30 years: 8.01% annualized return

If you combine this analysis with the current company’s payout and cash payout ratio, you should have a very good idea if management has enough room to continue their last 5 years growth rate or not. MMM currently shows a payout rate of 50.78% and a cash payout rate of 50.92%. Last year, MMM rose its dividend by 5.85% and the year before, the growth rate was of 8.29%. You can then see that the 5 year dividend growth rate isn’t going to be a good choice for the next 10 years.

A more reasonable growth rate of 8% sounds more appropriate. As a terminal growth rate, I rather go with conservative values. In this case I think it’s fair to assume MMM can keep a 6% growth rate considering its 30 years annualized growth rate being 8%.

Various discount rates applicable

There are various discussions about which discount rate to use. I mean, what kind of investing return do you want? Or do you expect? This question leads to a very subjective answer. If you are being too generous (e.g. looking for low discount rate), you will find the whole market is on sale all the time. On the other side, if you are being too greedy (e.g. looking for a high discount rate), you will never buy anything… but value trap!

The Fix:

According to financial theory, we should be using the Capital Asset Pricing Model (CAPM). This is another formula used to describe the relationships between the risk of an investment and its expected return:

As you can see, to determine the discount rate, you now have to determine several other variables. The Risk Free return refers to the investment return where there is virtually no risk. It is usually referred to the 3 months T-Bill return. As of August 4th 2017, Ycharts shows the 3 month T-Bill rate at 1.06%.

Going forward, the beta determines how a security fluctuates compared to the overall market. A beta less than 1 means the security fluctuate less than the market and vice versa. You can easily find stock beta on free websites such as Google Finance. For example, MMM beta is set at 1.06 as at August 4th 2017.

Now, the last metric to be used is the expected return of the market. This number could be widely debated. If you look at the S&P 500 total return over the past 5, 10 and 20 and 30 years, you get completely different numbers:

- 5 years: 14.63% annualized return

- 10 years: 7.93% annualized return

- 20 years: 6.89% annualized return

- 30 years: 9.90% annualized return

I would tend to discard the 5 year and 30 year results. The last 5 years don’t include a full economic cycle while things were a lot different back in 1987 and I don’t think we can expect such growth in the future. I guess the answer lies between the 20 and 10 years. To be fair, let’s use the average of both; 7.41%.

Here what should be the discount rate: 7.79% = 1.06% + 1.06*(7.41%-1.06%)

This is Quite a sensitive model

We are now ready to use our double-stage DDM and see if MMM is trading at an interesting value or not. Using the numbers described in this article, we have the following data:

| Input Descriptions for 15-Cell Matrix | INPUTS |

| Enter Recent Annual Dividend Payment: | $4.70 |

| Enter Expected Dividend Growth Rate Years 1-10: | 8.00% |

| Enter Expected Terminal Dividend Growth Rate: | 6.00% |

| Enter Discount Rate: | 7.79% |

Then, running the calculation will give us a fair value at $331.30…

| Discount Rate (Horizontal) | |||

| Margin of Safety | 6.79% | 7.79% | 8.79% |

| 20% Premium | $907.05 | $397.56 | $253.41 |

| 10% Premium | $831.46 | $364.43 | $232.30 |

| Intrinsic Value | $755.87 | $331.30 | $211.18 |

| 10% Discount | $680.29 | $298.17 | $190.06 |

| 20% Discount | $604.70 | $265.04 | $168.94 |

We will all agree MMM is NOT undervalued by 60% right now. The DDM is giving us a completely ridiculous value with a discount rate of 7.79%. Please note that I’ve selected dividend growth rates that are matching or below MMM 5, 10 , 20 and 30 years history. Therefore, I can’t really cut on those numbers already. However, if you look at the chart, my Excel spreadsheet gives me two more results according to a discount rate of 6.79% (-1%) and 8.79% (+1%). Interesting enough, the intrinsic value of $211.18 seems more appropriate already. But you can see how sensitive the model goes when 1% makes the difference between $755, $331 or $211 for the same stock.

The Fix:

The fix is obviously to put everything into perspective. Should I expect a higher market return and go back to my CAPM calculation? Because if my discount rate is closer to 9%, I get a valuation that is closer to what MMM is trading for. My fix for this problem is not to use the CAPM… huh? Yeah, you read it right, I use a different system based on the rest of my analysis.

Instead of using historical numbers and academic concept, I’ve decided to use 3 different discount rates according to the company’s situation:

9%: The company is well-established, a leader in its industry and shows stable numbers. Example: 3M co

10%: The company is well-established, a leader in its industry but shows an element of risk or fluctuation: Example: Apple (AAPL)

11%: The company shows important flaws or imminent menace to their business model. Example; could be Garmin (GRMN) since their core business (auto GPS) is melting

Then, by using my Excel spreadsheet, I have 3 different discount rate and 10% – 20% margins of safety calculated all at once. It helps giving the proper valuation to the company.

Final Thoughts

As you can see, we could all use the DDM on the same company and get several different answers. In the end, your valuation will be as good as your assumptions. Unfortunately, one point up or down in the calculation matrix and you can go from “BUY” to “SELL” in a heartbeat.

For this reason, it’s important to have a margin of safety and a range of calculation to give you a clear idea of whether you should buy, hold or sell the stock you analyze. The tool I use to calculate the DDM is found in The Dividend Toolkit. The Toolkit also includes a complete section on how to use the DDM and other valuation methods such as the Discounted Cash Flow model.

Finally, no matter how much time you spend on your valuation method, this will not likely be the reason of your success or failure as an investor. What will really determine if you can manage your own portfolio is your ability to develop a complete investing process and stick to it afterward. You can read about my detailed investing process here. It will give you a good head start!

This article was written by Dividend Monk. If you enjoyed this article, please subscribe to my feed [RSS]