Microsoft is the best known and most important software company in the world. Along with its famous line of software products, Microsoft also offers various services such as servers (including cloud systems), business solutions (support and consulting), entertainment (Xbox) and other online services.

-Seven Year Revenue Growth Rate: 9.71%

-Seven Year EPS Growth Rate: 8.23%

-Seven Year Dividend Growth Rate: 12.56%

-Current Dividend Yield: 2.55%

-Balance Sheet Strength: Strong

-Seven Year EPS Growth Rate: 8.23%

-Seven Year Dividend Growth Rate: 12.56%

-Current Dividend Yield: 2.55%

-Balance Sheet Strength: Strong

Overview

We all know Microsoft for their Windows operating system and Office Suite. At several occasions in time, we have seen competitors try to steal market share away from the giant. I remember watching an interview with the Microsoft CEO years ago and the reporter asked if he was concerned about the rise of Linux.

I was surprised to see MSFT’s big boss not even consider that a competitor could hurt Windows’ market share. Today, I understand that there is not many competitors can do to battle with the “mother” of computers.

The company is simply divided into two segments:

Devices & Consumer

Here we find all products offered to “regular” consumers.It showed an 8% growth in revenue during the past quarter lead by sales of Office 365. I was also surprised to see how BING posted strong revenue growth (21%) in advertising income.

Commercial

s consumers we all know Microsoft, while MSFT makes the bulk of its income from its commercial segment (12.8 billion this quarter vs 9 billion from consumer segment). Revenue in this segment grew 5% this quarter lead by… the cloud business (+106%). The cloud business is definitely a great part of MSFT’s future. This is especially true when we consider that office suite sales declined during the last quarter. Many companies won’t update their software bundle as fast as MSFT will upgrade them.

Ratios

Price to Earnings: 20.14

Price to Free Cash Flow: 14.93

Price to Book: 4.36

Return on Equity: 22.25%

Price to Free Cash Flow: 14.93

Price to Book: 4.36

Return on Equity: 22.25%

Revenue

Revenue Graph from Ycharts

Similar to Apple’s revenue depending on how many iPhones versions it launches; Microsoft revenue growth is linked to how many software upgrades it can create. We can see that MSFT is not lazy when it’s time to provide new versions of their famous software. On top of that, MSFT diversified its revenue sources by investing massively in two other business sectors; game consoles with the Xbox and cloud services.

Earnings and Dividends

Source: Ychart

Source: Ychart

Earnings were temporarily hit by the Nokia adventure. While MSFT usually shows strong abilities investing in new businesses in order to generate growth, I’m not truly convinced it will be able to get something strong out of Nokia. Nonetheless, it seems MSFT doesn’t need Nokia to be profitable since its other businesses are doing well. I guess this is the benefit of being the world leader in software.

Approximate historical dividend yield at beginning of each year:

As you can see, MSFT became very interesting as a dividend stock not so long ago. Prior to 2011, the yield wasn’t the most appealing. However, now the dividend is constantly increasing and the yield remains around 3%. Considering a relatively low payout ratio (under 50%), we can expect more dividend growth in the future.

How Does MSFT Spend Its Cash?

It’s funny to see a company that didn’t want to pay a dime in dividends a short while ago increase its dividend payment aggressively by 12.56% (annualized) over the past 5 years, right? During the last quarter alone, MSFT redistributed $7.5 billion to shareholders through share repurchases and dividend payments. The share repurchase program is authorized up to 40 billion dollars.

As any other techno companies, MSFT must invest massively into R&D. in 2014, the company spent 11.4 billion, an increase of 1 billion compared to 2013. Share repurchases and dividend payments are great, but I also like the fact MSFT is cautious about reinvesting massively into its operations. While MSFT focuses on improving existing products and services, they also spend lots of money on developing new innovation.

Investment Thesis

Microsoft finds another niche to dominate; here’s why the cloud business will push this giant higher. Both INTC and MSFT surged this year and even share a few points in common; strong demand for PCs in the market and their weakness to enter the mobile market. Microsoft also tried to “buy” its entry into the mobile market with the acquisition of Nokia. Now that they have announced a cut of 18,000 jobs (mainly in the Nokia division), we can wonder why it paid that much to acquire a cheap phone maker. Nonetheless, I prefer Microsoft over Intel for one reason; MSFT has found another niche to dominate with the cloud business. We all know the strength of Microsoft lies with all businesses using their services (Windows, Office series but also servers and business services). Since the cloud is the next big thing for most companies, Microsoft can expect huge growth from this segment in the future.

Risks

A few years ago, I wasn’t as confident in Microsoft’s future; the Xbox wasn’t doing that well, BING seemed like just another Yahoo! trying to compete with Google and Windows’ sales weren’t impressive. However, a few years later, BING generates revenues, Xbox is a strong player in the gaming industry and cloud services came out of nowhere with great growth potential. I guess this summarizes the risk you face while investing in a techno stock.

Overall, I think the risk is minimal since MSFT sits on strong and diversified sources of income. The software business will continue to generate strong cash flow while the growth will come from cloud services and other projects. Still, keep in mind that if MSFT wastes money like it did with Nokia, the future could turn rapidly into a nightmare.

Conclusion and Valuation

Using the historic price-earnings ratio will tell me how the market values MSFT over time:

My understanding of this graph is that MSFT is catching the attention of Mr. Market recently. The cloud business is a buzz word and it resonates throughout the MSFT valuation. Considering the company used to trade over a 22 multiple and as high as 27, the stock seems underpriced at the moment. Do we have a buy opportunity? The answer is probably yes… about a month ago! Let’s dig further.

Using the Discounted Cash Flow Analysis, we look at MSFT as a simple money making machine. The point is to assess the value of the company by considering its cash flow generation capacity. Considering the cash flow to continuously grow by 5% for the next five years and then by 4% and a discount rate of 10%, we have a stock trading at a 20% discount as the current company’s market value is at 392 billion.

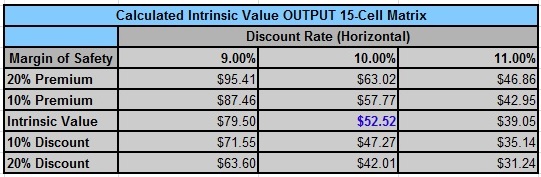

Then, by using the Dividend Discount Model, I keep the 10% discount rate and use a 10% dividend growth for 10 years (definitely supported by the cloud service growth and the upcoming delivery of Windows 10) and a 7% dividend growth rate afterward. Here’s what we get:

According to this chart, the stock is trading at a 10% discount.

Overall, it seems that Microsoft is currently trading at a good price. The perfect time was definitely before its latest earnings report, but I’m fairly confident that the stock will continue to show strong results in the future.

Full Disclosure: As of this writing, I MSFT is part of our DSR Portfolios.

This article was written by Dividend Monk. If you enjoyed this article, please subscribe to my feed [RSS]

This article was written by Dividend Monk. If you enjoyed this article, please subscribe to my feed [RSS]