Special note: Today, we have a guest post by Ben. He writes for Sure Dividend and he’s sharing an article about four excellent stocks and how they rank within the framework of his “8 Rules of Dividend Investing”. I don’t allow guest posts very often, and Ben and I have been in discussion about this article for more than a month now. But he took a lot of time to put this post together and I think there’s some real value here. In addition, I spent considerable time formatting everything. I hope everyone enjoys it!

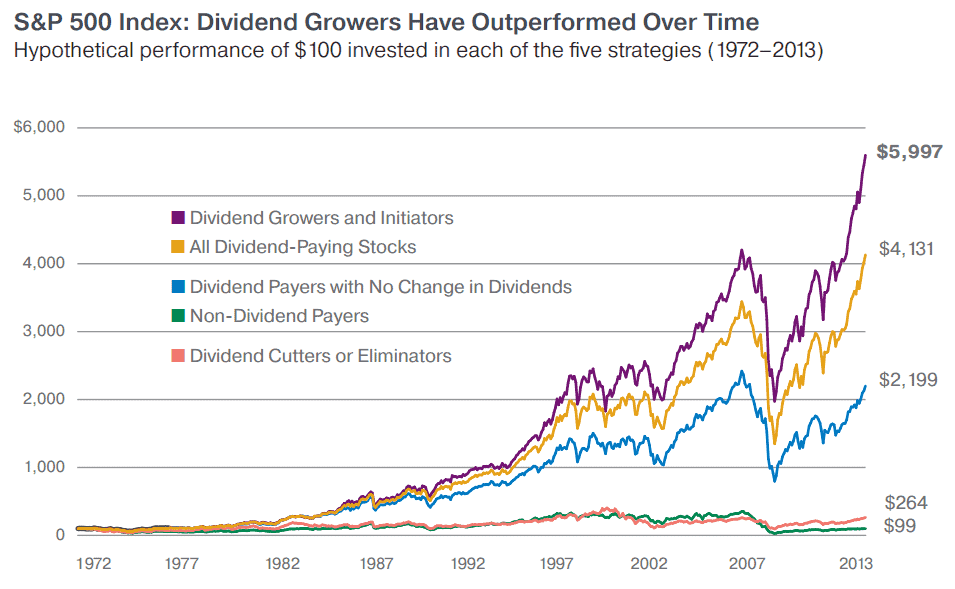

Dividend growth stocks make an excellent choice for investors seeking both income and growth. Dividend growth stocks raise their dividend year after year, growing their owner’s income streams. Who doesn’t want a rising standard of living year after year? Not only do dividend growth stocks have practical appeal, they have also historically outperformed non-dividend paying stocks by about 7.8 percentage points per year from 1972 through 2013.

Not a bad excess return, for simply buying stocks that raise their dividends year after year.

Source: Oppenheimer Rising Dividends

Don’t Overpay

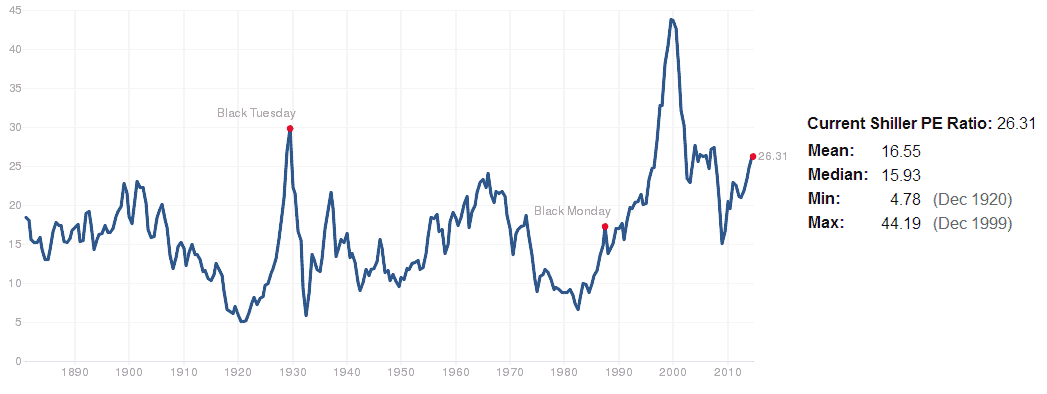

It is not always a great time to buy dividend growth stocks. The trick is to buy when dividend growth stocks are trading at fair or better prices. Unfortunately, the stock market is overvalued at this time. The Shiller P/E ratio (or PE 10), which measures the current price of the market divided by average earnings over the last 10 years, shows the market is near the same valuation levels of the 2007 crash. The only time the stock market has been more overvalued than today, outside of the late nineties and 2000’s, is just before the Great Depression, in 1929. These are scary times for stock investors.

Source: Multpl.com

Many dividend growth stocks have taken part in the market rally, and are now overvalued. Buying stocks trading at high P/E multiples has historically diminished investor returns. On the other hand, buying high quality dividend growth stocks at fair value or less than fair value is an excellent way to build long-term wealth.

“It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

– Warren Buffett

Despite the overvalued market, there are still several dividend growth stocks that I believe are trading for fair value or less, and offer income growth, safety, and stability for investors willing to hold through the ups and downs of the stock market.

This article will take a look at four businesses I believe are trading at fair or better prices. The current events of each business will be examined below, along with what has made them bargains. Finally, each business’ dividend attractiveness will be analyzed using the 5 Buy Rules from the 8 Rules of Dividend Investing.

Undervalued Retail King: Wal-Mart

Wal-Mart is the world’s largest retailer, and 11th largest publicly traded company. The company is trading at a substantial discount to its historical PE 10 ratio.

Source: Ycharts

Wal-Mart’s stock is depressed because it has shown lackluster performance in recent history. Wal-Mart has not increased comparable store sales in its flagship US Wal-Mart stores since the fourth quarter of the company’s fiscal 2013. Sam’s Club has fared better than Wal-Mart US, but has still seen mediocre comparable store sales growth. The company had flat comparable store sales growth this quarter, following 2 consecutive quarters of declines.

| Comparable Store Sales | |||

| Quarter | Wal-Mart US | Sam’s Club | |

| 2015 Q2 | 0.00% | 0.00% | |

| 2015 Q1 | -0.01% | -0.50% | |

| 2014 Q4 | -0.40% | -0.10% | |

| 2014 Q3 | -1.30% | 1.10% | |

| 2014 Q2 | -0.30% | 1.70% | |

| 2014 Q1 | -1.40% | 0.20% | |

| 2013 Q4 | 1.00% | 2.30% | |

Despite this weakness, Wal-Mart appears to be reversing its negative comparable same store sales trend. The company posted its first non-negative Wal-Mart US comparable store sales growth numbers in 6 quarters in its most recent quarter.

Wal-Mart’s International division had significantly better comparable store sales results than its US based operations this quarter. Brazil in particular has done well this year, achieving double-digit comparable store sales growth through the first half of Wal-Mart’s fiscal 2015. The company’s comparable store sales for its top 5 international markets are shown below.

| Comparable Store Sales | ||||||

| Quarter | UK | Canada | Mexico | Brazil | China | |

| 2015 Q2 | 2.00% | 1.90% | 0.20% | 9.70% | -1.60% | |

| 2015 Q1 | -1.50% | -2.60% | -1.40% | 4.40% | -2.50% | |

Wal-Mart’s Domestic Improvement Plans

Wal-Mart is not standing idly by and watching its US comparable sales stagnate. The company’s neighborhood market stores show promise; comparable store sales were up 5.6% in the most recent quarter. Neighborhood market stores are about one quarter the size of Wal-Mart super center stores. They are the discount retailer’s answer to grocery stores. Wal-Mart is on track to open between 180 and 200 new neighborhood market stores in the US this year.

Wal-Mart has had success with smaller stores. The company has plans to open about 90 Wal-Mart express stores in its fiscal 2015. These stores are about one tenth the size of Wal-Mart super centers by square footage. These stores will offer gas, a pharmacy, and discount pricing. They combine the convenience of a gas station corner store, the health focus of a drug store, and the discount pricing of a dollar store. Wal-Mart can leverage its tremendous scale to offer cheaper goods at its smaller stores than other dollar store and discount retail competitors. The express store concept will allow Wal-Mart to “fill in the gaps” between its larger super center stores, opening up a new growth market for the company in the US.

Wal-Mart & E-Commerce

Wal-Mart grew e-Commerce sales 24% year over year for the second quarter of 2014. The company managed to gain market share in the competitive U.S. e-Commerce market. Wal-Mart recently released its Savings Catcher which gives customers the difference of prices on items purchased at Wal-Mart if Wal-Mart did not have the lowest price. The savings catcher is another way to tell customers “we have the lowest prices, and we will prove it to you”.

In addition to double digit e-Commerce growth in the US, Wal-Mart also saw double digit e-Commerce growth in Brazil, Mexico and Chile. More impressively, Wal-Mart saw triple digit revenue growth in Canada and Argentina. The company is bolstering its e-Commerce division by acquiring talented workers through buying out smaller tech businesses. Recent acquisitions include Adchemy, Stylr, and Luvocracy. Wal-Mart is expecting e-Commerce sales to grow by 25% over its full fiscal 2015.

Highly Disciplined Insurer Chubb Group

Chubb Group is an insurer that sells home, car, business, and supplemental health policies. The company sells insurance through independent agents and brokers throughout North and South America, Australia, Europe and Asia. In the first half of 2014, about 77% of Chubb’s premium revenue came from the US and 23% came internationally.

Chubb Group does not trade at the lofty P/E ratios that many other high quality dividend growth stocks do at the moment. The company has a P/E ratio of 11.4, versus the market’s P/E ratio of 18.2.

Sluggish Second Quarter Results Hide True Value

Chubb Group’s net income dropped 8% for its most recent quarter compared to the same quarter a year ago. On the positive side, Chubb increased its premium revenue 5% on a constant currency basis versus the same period last year. US premium revenue increased 5%, and international premium revenue grew 1%. Property and casualty investment income declined 4% versus the same quarter a year ago.

Chubb breaks its business into 3 reporting divisions: Chubb Personal Insurance, Chubb Commercial Insurance, and Chubb Specialty Insurance.

Chubb Personal Insurance

- Net written premiums up 5%

- Combined ratio excluding catastrophic losses up to 85.2% from 76.9% in 2nd quarter of 2013

- 38% of second quarter 2014 revenue

Chubb Commercial Insurance

- Net written premiums up 3%

- Combined ratio excluding catastrophic losses up to 88.4% up from 81.8% in 2nd quarter of 2013

- 42% of total second quarter 2014 revenue

Chubb Specialty Insurance

- Net written premiums up 5%

- Combined ratio down to 78.7% from 86% in the 2nd quarter of 2013

- 20% of total second quarter 2014 revenue

Underlying Business Is Still Growing

Chubb’s negative earnings per share growth is due to lower investment income and a higher combined ratio. The combined ratio is the sum of business expenses and claims paid divided by premium revenue. The lower the combined ratio, the better.

The underlying business grew 5% on a constant currency basis based on the amount of premiums written. Despite the drop in earnings per share, the company is still on a growth trajectory.

Investment income and the combined ratio fluctuate on a yearly basis and do not reflect underlying business growth. The increase in the combined ratio is not cause for alarm, as it is still well under 100% meaning the company is doing an excellent job of writing profitable policies.

Chubb’s competitive advantage comes from its disciplined underwriting approach. The company reported a combined ratio well under 100% for the 2nd quarter of 2014. Chubb has not had a year with a combined ratio over 100% since 2002.

Source: Chubb 2013 Annual Report

Chubb Group Is Buying Itself

Chubb repurchased nearly 6% of its shares outstanding over the last year, boosting shareholder return. The company has historically been a strong share repurchaser. Chubb Group is repurchasing its shares when it is arguably undervalued, returning more value via share repurchases than would be realized if the company were fairly valued or overvalued. Chubb has traded at a low PE 10 ratio since 2009.

Source: YCharts

Chubb’s future growth prospects are strong in the US. The company’s disciplined underwriting allows it to steal market share from less conservative insurers due to the fluctuations in the insurance industry. When the insurance market is highly competitive, Chubb writes less policies while its competitors write policies at a loss. When these unprofitable policies cause a contraction in the company’s competitors, Chubb is there to increases its market share.

Fast-Food Leader McDonald’s is Cheaper than Its Value Menu

McDonald’s is arguably the most recognizable restaurant brand in the world. It is certainly the largest publicly traded restaurant, with a market cap of $93 billion. Its closest competitor (Yum! Brands) has a market cap of $30 billion, almost 3x as small as McDonald’s. McDonald’s operates or franchises nearly 35,000 restaurants throughout the globe. The company trades at a P/E ratio of 16.15, well below the market average of 18.2.

Recent McDonald’s Results Are Unsatisfying

McDonald’s grew constant currency revenues 1% for the second quarter of 2014 compared to the 2nd quarter of 2013. The company’s same store sales were flat. Revenue growth was driven entirely by increasing store count.

McDonald’s comparable store sales decreased 1.5% in the US. Declining sales resulted from strong competition in the fast food industry and a slowly changing consumer preferences. The company plans to turn negative US sales growth around by enhancing customer service and focusing the menu on its core offerings. The McDonald’s menu has substantial room for improvement. One glance at McDonald’s menu will show that the company has opted to clutter its menu rather than provide clear, simple options.

McDonald’s European restaurants saw comparable store sales decrease 1%. On a country by country basis, the U.K. and France delivered strong results, while German McDonald’s stores fared poorly. The company rolled out blended ice beverages in Europe for the quarter which lessened the impact of unfavorable results in Germany.

Sales in McDonald’s Asia/Pacific, Middle East, and Africa (APMEA hereafter) region were the company’s bright spot. Comparable store sales increased 1.1% due to strong growth in China. The APMEA region posted positive same store sales growth despite weakness in Japan. Since the 2nd quarter earnings release, the company has seen a big pullback in the Asia/Pacific region in general and China in particular due to a Chinese supplier selling tainted meat. The bad publicity from this event caused McDonald’s comparable store sales in the APMEA region to plummet 14.5% in August. This is a one time event that has created a better entry point for investors in McDonald’s. Once the company recovers from the tainted meat debacle in China, it will see continued growth in the APMEA region.

Geographically, McDonald’s is seeing its comparable store sales fall in the developed world. The US, Europe, and Japan all saw negative comparable store sales growth. McDonald’s has historically peformed much better in the developing world (not counting the recent Chinese tainted meat fiasco).

Developed market weakness is most likely temporary. McDonald’s managed to comparable store sales in the developed world significantly over much of the last decade. The business has the opportunity to test new concepts at a small portion of its stores and roll out beneficial changes to the bulk of its stores.

McDonald’s announced plans to return between $18 billion and $20 billion to shareholders over the next three years through dividends and share repurchases. This is about a 6% annualized return over the next 3 years. The company’s phenomenal cash flows allow it to return the bulk of its money to shareholders while still investing in growth.

McDonald’s 2nd quarter results were not fantastic, but they are not cause for alarm. The company needs to find a way to fix weakness in the developed world and control the situation in APMEA. When it does, it will be able to grow revenue faster than the ~3% a year it is currently generating from store expansion. All in all, shareholders of McDonald’s can expect near double digit returns without same store improvements from dividends, share repurchases, and new store openings. Increasing comparable store sales will just be icing on the cake (or special sauce on the Big Mac).

Exxon Mobil: The Leader in Black Gold

Exxon Mobil is the largest publicly traded oil and gas corporation in the world, and second-largest publicly traded corporation overall, based on its market cap of over $386 billion. Exxon Mobil’s lineage goes back to the original dominant oil company: Rockefeller’s Standard Oil, which was founded in 1870.

As the world’s largest oil corporation, Exxon Mobil is the embodiment of Standard Oil today. Exxon Mobil has the record for the highest profit ever recorded in any year by a corporation ($45.22 billion in 2008). The company is extremely profitable, and has a long history of rewarding shareholders through growing dividends.

Oil Fears Lead To Undervaluation

Exxon Mobil’s P/E ratio is only 11.5. The company’s P/E 10 ratio has barely recovered from the Great Recession of 2007 to 2009, and is well below the company’s historical average.

Source: YCharts

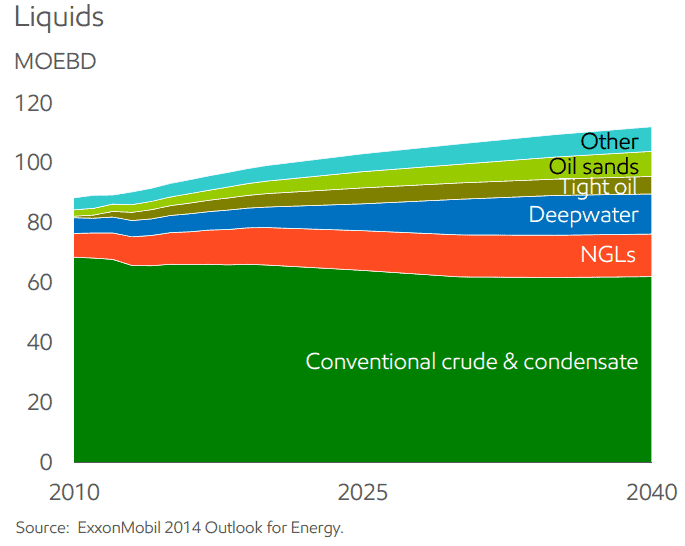

Exxon is likely undervalued due to fears about the future of the oil industry, making now a good time to start a position in the stock. Many people believe oil will be supplanted by renewable forms of energy such as solar and wind. While these forms of energy are growing faster than oil energy, the world still runs on oil. It is likely that energy demand for oil will continue to rise for the next several decades. Sure, I can’t see the future (let me know if you can!), but there is simply not enough evidence to say that the oil industry will become obsolescent more quickly than any other industry around today.

Rising Energy Demand

Exxon Mobil’s future growth will come from rising global energy demand. Global energy demand is expected to steadily trend upward due to population growth and rising GDP in developing markets. Demand growth from the population and broadening middle classes in emerging markets will be partially offset by efficiency gains from advancing technology and ‘austerity’ and environmental movements in developed markets.

Oil and gas will provide the bulk of energy the world demands for the foreseeable future. Solar, wind, and biofuel energy sources are expected to grow at nearly 6% a year over the next several decades, compared to less than 1% and 2% average expected growth for oil and gas, respectively. Despite higher growth rates, renewable energy is still projected to make up only a small fraction of total energy use over the next several decades.

There is only a finite supply of oil and gas on earth. Technological advances have made it possible for Exxon Mobil (and its competitors) to find and produce oil that would have been impossible or uneconomical in the past. Examples of previously difficult or impossible production sites are the oil sands and various deep water sites around the globe. In addition, hydraulic fracturing (fracking) is creating a renaissance in the US oil industry. Additionally, hydraulic fracturing will open up further oil reserves outside of North America.

Exxon Mobil Earnings Continue to Grow

Exxon Mobil’s earnings increased from $6.86 billion in the second quarter of 2013 to $8.78 billion in the second quarter of 2014. The company earnings increased in all 3 of its divisions: Upstream, Downstream, and Chemical.

The company’s upstream division grew earnings by $380 million as compared to the 2nd quarter of 2013, not counting a large one-time gain of $1,190 million from asset sales in Hong Kong. Exxon’s upstream division is responsible for the bulk of the company’s profits. In the second quarter of 2014 the upstream division accounted for over 83% of income.

Comparing XOM, CB, MCD, & WMT

Each of the businesses analyzed above are analyzed below using the 5 buy rules from the 8 Rules of Dividend Investing. Each rule uses quantitative rules that have historically increased returns using verifiable research. The goal is to find high quality businesses that reward shareholders with increasing dividends year after year suitable for long-term holding.

Rule #1: Long Dividend History

A long history of dividend increases shows the durability of a company’s competitive advantage. All of the businesses mentioned in this article have paid increasing dividends for over 25 years. Each businesses dividend history is listed below.

- Wal-Mart – 41 consecutive years of dividend increases

- Chubb Group – 32 consecutive years of dividend increases

- McDonald’s – 37 consecutive years of dividend increases

- Exxon Mobil – 32 consecutive years of dividend increases

Why it matters: The Dividend Aristocrats (stocks with 25-plus years of rising dividends) have outperformed the S&P 500 over the last 10 years by 2.88 percentage points per year.

Rule #2: Dividend Yield Rank

McDonald’s is the only business on the list with a dividend yield in excess of 3%. The other companies all have dividend yields higher than the S&P 500. The rank of each businesses’ dividend yield out of 132 businesses with 25+ years of dividend payments without a reduction is shown in the picture below.

- Wal-Mart has a dividend yield of 2.46%

- Chubb Group has a dividend yield of 2.15%

- McDonald’s has a dividend yield of 3.73%

- Exxon Mobil has a dividend yield of 3.05%

Why it Matters: Stocks with higher dividend yields have historically outperformed stocks with lower dividend yields. The highest-yielding quintile of stocks outperformed the lowest-yielding quintile by 1.76 percentage points per year from 1928 to 2013.

Rule #3: Payout Ratio Rank

None of the businesses discussed in this article have an excessive payout ratio. Businesses with low payout ratios have more remove to increase dividend payments at a faster rate than overall company growth which provides further benefit for income oriented investors.

- Wal-Mart has a payout ratio of 37%

- Chubb Group has a payout ratio of 27%

- McDonald’s has a payout ratio of 56%

- Exxon Mobil has a payout ratio of 35%

Why it Matters: High-yield, low-payout ratio stocks outperformed high-yield, high-payout ratio stocks by 8.2 percentage points per year from 1990 to 2006.

Rule #4: Growth Rate Rank

Surprisingly, Wal-Mart has managed to grow revenue per share at more than 8% a year over the last decade. All of these businesses have grown revenue per share at a clip faster than 6% over the previous 10 years.

- Wal-Mart has a 10 year growth rate of 8.2%

- Chubb Group has a 10 year growth rate of 6.4%

- McDonald’s has a 10 year growth rate of 7.1%

- Exxon Mobil has a 10 year growth rate of 6.3%

Why it Matters: Growing dividend stocks have outperformed stocks with unchanging dividends by 2.4 percentage points per year from 1972 to 2013.

Rule #5: Volatility Rank

Businesses with low standard deviations have more stable stock prices, and generally more stable cash flows. Low volatility stocks help investors sleep better at night, as they typically see lower price declines in recessions (and lower gains in bull markets).

- Wal-Mart has a 10 year standard deviation of 19%

- Chubb Group has a 10 year standard deviation of 27%

- McDonald’s has a 10 year standard deviation of 20%

- Exxon Mobil has a 10 year standard deviation of 25%

Why it Matters: The S&P Low Volatility index outperformed the S&P 500 by 2 percentage points per year for the 20-year period ending September 30th, 2011.

Source: Low & Slow Could Win the Race

Ending Thoughts

It is becoming increasingly difficult to find high quality dividend growth stocks trading at fair or better prices in today’s overvalued market. Wal-Mart, McDonald’s, and Exxon Mobil are all ranked in the Top 10 out of 132 stocks with long histories of dividend payments based on the 8 Rules of Dividend Investing. Chubb Group is ranked in the Top 20. These four businesses are all high quality, low risk companies with long histories of rewarding shareholders through increasing dividends. They all operate in relatively slow changing industries, and are likely to continue to increase dividend payments at a rate significantly faster than inflation over the next several years. Further, they may see additional gains if their P/E multiples rise to match the quality of the underlying business.

Full Disclosure: Dividend Mantra is long MCD, WMT, and XOM. Sure Dividend is long MCD and WMT.

Thanks for reading.

What did you think? Do you like his methods on ranking stocks? Let us know!This article was written by Dividend Mantra. If you enjoyed this article, please subscribe to my feed [RSS]