Summary:

15% CAGR dividend growth rate over the past 5 years and the company still has plenty of room to reward investors.

Both Revenues and Earnings show double digit growth over the past five years.

Strong management with conservative cost control approach makes this money making machine even stronger.

DSR Quick Stats

Sector: Industrial – Railroads

5 Year Revenue Growth: 11.22%

5 Year EPS Growth: 14.64%

5 Year Dividend Growth: 15.40%

Current Dividend Yield: 1.71%

What Makes Canadian National Railway (CNI (CNR.TO)) a Good Business?

Founded in 1918, Canadian National Railway is the largest railway in Canada and has significant operations in the United States. The rail network extends from the Atlantic to the Pacific Ocean through Canada, and also extends southward to the Gulf of Mexico through the United States. The total mileage of track exceeds 20,000. The company trades on both Canadian and US markets under CNR.TO and CNI tickers.

The company is divided into seven commodity groups:

-Petroleum and Chemicals

-Metals and Minerals

-Forest Products

-Coal

-Grain and Fertilizers

-Intermodal

-Automotive

Ratios

Price to Earnings: 16.08

Price to Free Cash Flow: 26.60

Price to Book: 3.934

Return on Equity: 24.06%

Price to Free Cash Flow: 26.60

Price to Book: 3.934

Return on Equity: 24.06%

Revenue

Revenue Graph from Ycharts

Revenue Graph from Ycharts

Revenues were slightly lower in 2015 for the first time since 2010 due to less economic activity around coal, grain and crude oil. The global shift toward cleaner energy will continue to hurt the demand for coal, but the company should benefit from higher activity in the forest industry since the CAD is ever lower compared to the USD.

How CNI (CNR.TO) fares vs My 7 Principles of Investing

We all have our methods for analyzing a company. Over the years of trading, I’ve been through several stock research methodologies using various sources. This is how I came up with my 7 investing principles of dividend investing. The first four principles are directly linked to company metrics. Let’s take a closer look at them.

Source: Ycharts

Source: Ycharts

Principle #1: High dividend yield doesn’t equal high returns

I’m usually not a big fan of high yield dividend stocks, but I’m not a huge fan of low yield dividend stocks either. Financial research has proven that stocks with yield in the 2nd highest quartile outperform the others. Therefore, my target for a strong dividend stock is usually between 2% and 5%. CNI fails to meet this requirement:

Source: data from Ycharts.

Source: data from Ycharts.

On the other hand, the dividend growth is quite impressive. This is why I have decided to look into this company further.

Principle#2: If there is one metric, it’s called dividend growth

Speaking of dividend growth, CNI is probably one of the best examples of a Canadian dividend growth stock. By the nature of its business model, railway companies produce important levels of cash flow leading to strong ability to increase dividend payouts. Over the past 5 years, the company has a dividend growth rate over 15% annually. At this rate, the dividend payment will double every 5 years.

Such strong dividend growth perspective is fueled by ever increasing revenues and profits. Without such a strong base, a company wouldn’t be able to open the dividend reservoir that wide.

Principle #3: A dividend payment today is good, a dividend guaranteed for the next ten years is better

The real question is; can Canadian National Railway keep increasing its dividend at this pace? Here is how the dividend payment and the payout ratio have looked like over the past 10 years:

As you can see, the payout ratio is steadily increasing from a low of 16% in 2007 to 27% in 2015. However, the company could easily keep up with a 10% dividend increase for several years with such low payout ratio.

Principle #4: The Foundation of dividend growth stocks lies in its business model

The company’s business model is strong as they serve many different industries. This makes CNI able to switch from coal, grain and crude transportation to lumber & panels, chemistry and automotive transportation in a heartbeat.

The company’s cash flow generating ability has been envied by its peers for years and this makes CNI dividend growth base more solid than rock.

What Canadian National Railway Does With its Cash?

There is nearly 20% of CNI revenue used for railway maintenance. This is probably the biggest downside of such companies is the high cost of maintenance. As trucks can use “free roads” and pipelines require less maintenance, railway companies must take care of their own track.

However, the company is generating over 2 Billion in free cash flow per year. In 2015, the company uses this cash flow to increase the dividend payment by 25%. Management goal is to reach 35% payout ratio in the upcoming years, opening the door for more dividend increases.

Investment Thesis

Railroads serve a critical role in world transportation. They remain the most energy efficient way of transporting large amounts of material far distances. From an investing point of view, railways also have among the very strongest of economic moats, in that they are established businesses where new competitors are scarce. Obstacles to starting up a new railway business are obvious, because once track is put down to serve an area, duplicate track would be a poor investment.

The company has several strong indicators:

-None of the seven commodity groups account for more than 20% of revenue, which is solid diversification.

-Further evidence in terms of diversification; 18% of revenue comes from U.S. domestic traffic, 22% comes from Canadian domestic traffic, 28% comes from trans-border traffic, and 32% comes from international traffic.

Overall, I view Canadian National Railway as a fundamentally solid, albeit cyclical, business. The revenue growth is consistent, free cash flow is fairly strong, and the balance sheet is healthy. The business portfolio has satisfactory diversification and breadth in terms of geography and commodity groups. Railways have natural moats surrounding their businesses. A simultaneous pro/con is that capital expenditure is very regular and increasing. It shows that management is on top of their priorities for long-term sustainable growth, efficiency, and safety, but when this outpaces revenue growth, there is of course a cost.

Risks

The company is fairly safe from competitors in my view, so the risks are mainly associated with macroeconomic conditions. The company held up well during the recession but was still materially impacted by it, and this will likely be the case during the next recession as well, whenever it occurs. The company has good safety metrics and as previously mentioned, spends considerable sums on capital expenditures, so catastrophic incidents should be rare. My view is that the company is cyclical, but fundamentally solid on all observable quantitative and qualitative matters.

The global slow down for various commodities at the same time might affect revenues in the near-term but the railways will still be there to benefits from the next economic boom.

Should You Buy CNI (CNR.TO) at this Value?

Now, usually stellar companies command a premium on their stock price. Is it the case for CNI? Let’s take a look at the past 10 years PE ratio to see how the market values the company:

The latest correction in the market seems to have created a very interesting entry point in CNI. The company seems fairly valued at a PE ratio around 16 if we compared the past 5 years.

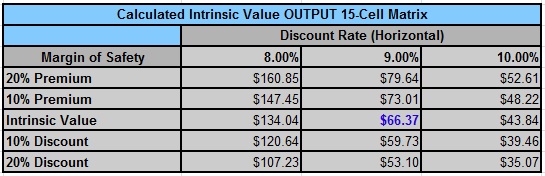

Since I’m a dividend growth investor, I will also consider the company as a pure money making machine by using the dividend discount model. Since CNI evolves in a fairly stable and predictable market, I will use a discount rate of 9%. As for dividend growth, I use a 10% rate for the first 10 years and reduce it to 7% to be more conservative.

As you can see, while the stock price has gone up by 77% over the past 5 years, there is still room for more growth. The company is currently undervalued by over 10% which is definitely a great entry point. This gives a good margin of safety for someone considering buying the stock at this time.

Final Thoughts on CNI (CNR.TO) – Buy, Hold or Sell?

Canadian National Railway is not paying the highest dividend yield on the market (1.76%) but it is continuously increasing its payout (400% total increase over the past 10 years) while maintaining a payout ratio under 30%. There is limited competition in this sector and CNR is often cited as one of the best managed railway company in North America. For more conservative investors, CNR will bring more stability coupled with better dividend growth perspectives.

Disclaimer: I hold shares of CNI in our DividendStocksRock portfolios

This article was written by Dividend Monk. If you enjoyed this article, please subscribe to my feed [RSS]