Qualcomm has been on my radar for a while now. More recently, a legal lawsuit coming from Apple (AAPL) made QCOM stock price drop by over 10% since the beginning of the year. It seems a great entry point for any investors looking to had a techno dividend paying company.

Qualcomm Inc develops digital communication technology called CDMA (Code Division Multiple Access), & owns intellectual property applicable to products that implement any version of CDMA including patents, patent applications & trade secrets. The company derived most of its income from the smartphone business selling chips for power and network connectivity.

Main strengths:

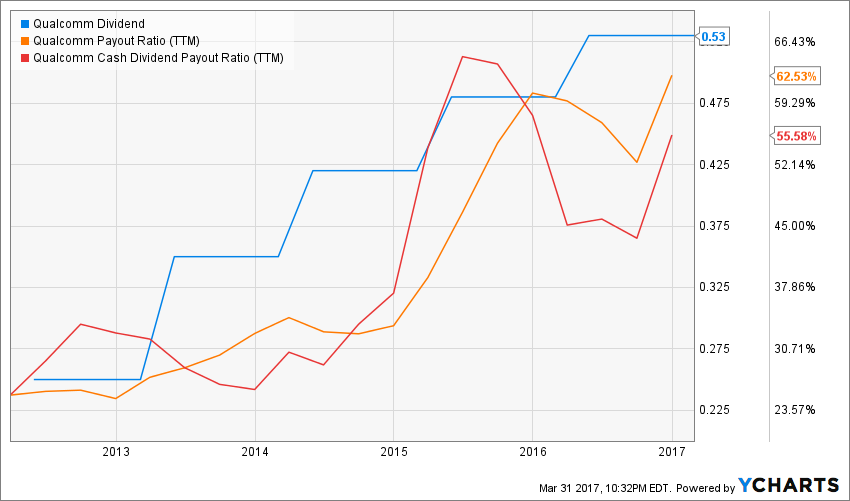

QCOM rides naturally on the smartphone wave as 90% of its revenues is derived from this industry as it drives royalty from 3G and 4G utilization. We see another great year for the smartphone industry in 2017, therefore, Qualcomm should continue to benefit from this profitable business niche. QCOM has implemented both buybacks and dividend payment increases at the same time.

Potential risks:

On top of China, other governments are eyeing QCOM business model under the anti-monopoly regulations. This could hurt future royalty earnings and therefore reduce QCOM growth potential. QCOM owns near to a monopoly in CDMA technology patent which is why it can charge such high royalty fee (3-5%). Worst case scenarios include a diminution of royalty fees which would affect QCOM future earnings growth.

Dividend growth perspective:

QCOM business model benefits from very strong royalty generated through patents. Those patents will generate strong cash flow for the next decade to come. This money will definitely results in additional dividend increase in the future. The company has a great window to find other opportunities while it enjoys its royalties. The dividend payment should continue to grow steadily in the upcoming years.

Investment thesis:

As we believe royalties will continue to bring in the dough for a decade, QCOM is sitting on a sustainable business model giving it the possibility to grow even bigger. In 2016, the company has gained strong momentum on the stock market and we believe this uptrend will persist in 2017. Its strong relationships with smartphone makers gives QCOM an edge about what is coming in the newest technology needs. You can bet QCOM will also own patents in the future mobile industry.

Valuation:

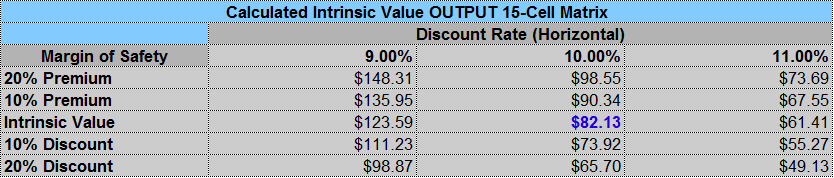

I’ve used the double stage dividend discount model to determine QCOM fair value. I believe in the strong potential of the company and the DDM shows there is a clear opportunity at the moment. Once the legal lawsuit with Apple (AAPL) is resolved, QCOM could rise again.

Disclaimer: Long AAPL, no position in QCOM yet.

This article was written by Dividend Monk. If you enjoyed this article, please subscribe to my feed [RSS]

This article was written by Dividend Monk. If you enjoyed this article, please subscribe to my feed [RSS]