It’s one of the biggest fears people have: outliving their money. An incredible 61% of baby boomers fear outliving their money more than they fear death! But so many are doing nothing about it or they’re simply not sure what to do.

Let’s first lay out the fundamental issue here. The problem is that most people will not have enough retirement income to cover their expenses.

It’s Not Easy to Generate Income in Retirement Today

Interest rates are historically low. That is probably the biggest problem when it comes to retirement income. With 30 year treasury yields barely beating inflation, how can anybody be expected to use bonds for retirement income?

It already almost seems like ancient history when most people could retire by age 65, move most of their money to treasury bonds, and sit back and enjoy the rest of their life without stressing out about their money. Simply stick to the budget that matches up expenses with interest income and all is well.

But that strategy is long gone now. It has become official policy of the Federal Reserve to keep interest rates low in order to push people into the stock market. Their thinking is that this will help prop up a fragile economy.

Bad theories aside, this is the world we live in now. Short of trying to get rid of the Federal Reserve, people need to take action.

Dividend-Growth Stocks for Retirement

Instead of low interest rate bonds or hidden-fee annuities, I recommend using dividend-growth stocks for generating enough income in retirement.

I have written before about how to retire early using dividend-growth stocks. They accomplish this by investing in great companies early on, and reinvesting the dividends.

The key is to find dividend payers who increase their dividends every year, even in recessions. At the very least, you don’t want companies that cut their dividend.

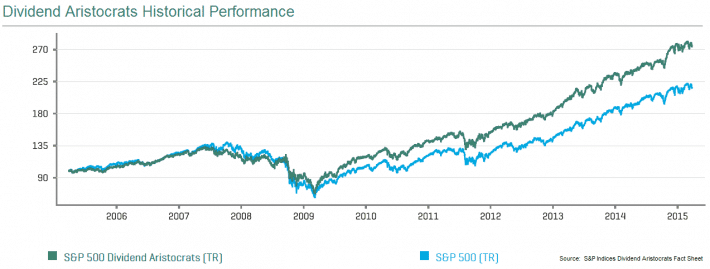

A good place to start your search for these companies is in the Dividend Aristocrats Index.

The companies in the Dividend Aristocrats Index are those which have increased their dividends by 25+ years in a row. These are seriously stable companies who have weathered many storms.

Digging Into the Numbers

Let’s take a look at an actual case study. I ran a sample case in the WealthTrace Financial & Retirement Planner, which is available to the public as well.

I want to look at a married couple that is 52 years old today. Their goal is to live off of income in retirement. Initially they think they can use Treasuries for this. In this example they are switching all of their money to Treasuries when they retire. My assumptions are below:

|

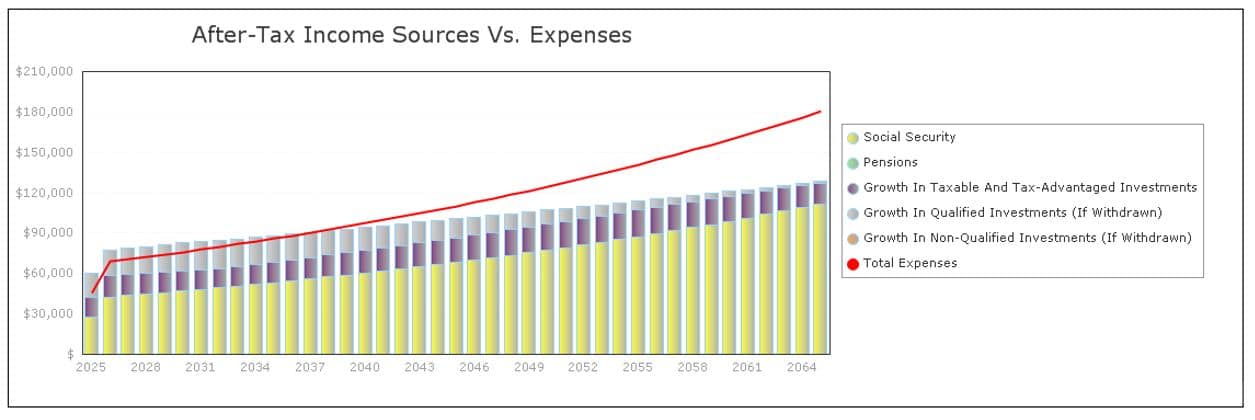

In the chart below you can see how their income in retirement is not keeping up with their expenses. This means they must be dipping into their investment principal.

Because they are dipping into their investment principal, they are projected to run out of money at age 86.

The Solution to This Problem

I propose moving half of their money to dividend-growth stocks. A few of my favorite dividend payers are Exxon (XOM), Altria (MO), Johnson & Johnson (JNJ), and Procter & Gamble (PG).

| Company | Div. Yield | 5 Year Div. Growth

Rate (Annualized)

|

| Exxon | 3.4% | 10.6% |

| Altria | 3.6% | 8.2% |

| Johnson & Johnson | 2.8% | 6.9% |

| Procter & Gamble | 3.3% | 7.5% |

Keep in mind that I’m not saying investors should only be in four stocks. Everybody should diversify. You need to find several companies that have characteristics like the companies highlighted here.

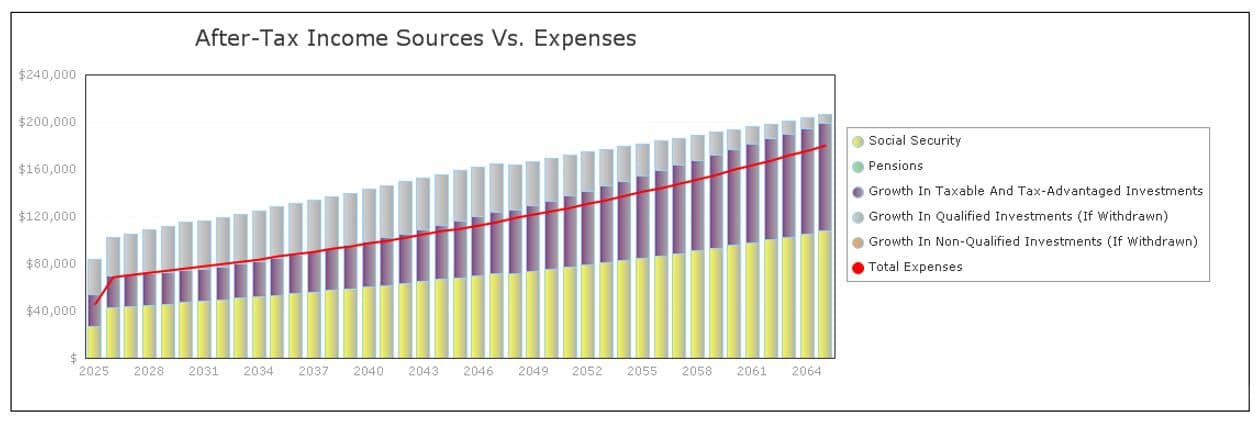

Let’s now take a look at their projections once we move half of their money out of Treasuries and into our dividend-growth stocks.

This is looking better. Their income in retirement is now covering all of their expenses. This is where they want to be. If income can indeed cover their expenses, they are in no danger of outliving their money.

It takes some time and effort to find great dividend payers that can set you up for retirement. But it is well worth the effort. There are few places to return for relatively stable (and sizable) retirement income. Solid dividend-growth stocks are one of the last, best remaining choices.This article was written by Dividend Mantra. If you enjoyed this article, please subscribe to my feed [RSS]