Well, the time has come to update the Freedom Fund once again as we start another month. The Freedom Fund is my portfolio, and I think it’s aptly named. My portfolio is my way to freedom; freedom from a job I don’t desire to purchase goods I don’t need to impress neighbors I don’t care about. This journey is all about freedom and flexibility. One day, the dividend income this portfolio generates will fully cover my expenses and my time will be completely my own. What could you possibly want to own more than your time?

I’m extremely fortunate that I’m able to post these updates every single month, which shows the power of monthly contributions to investments because of the high savings rate I maintain. It shows how a relatively large sum of money can be built through the power of time, patience and perseverance.

It’s important to keep in mind that while updating the overall value of my portfolio is important for historical reference and keeping track of total return, as well as giving context to the dividend income I earn, my main focus is on the rising dividend income stream the Fund provides.

I took the opportunity to add to a number of existing positions this month that, for one reason or another, appeared to offer compelling long-term value, especially after a few of them dropped somewhat substantially in price over a fairly short period of time. While there are a number of stocks I’m not actively interested in adding to due to exposure, I had a little room left for those stocks I did add to this month.

I’ll quickly note that I have a large chunk of free trades in my brokerage account, which is why you’ll notice a lot of smaller transactions below. I have historically tried to make sure transactions averaged somewhere around $1,400 to limit commission fees, but I paid almost nothing in commissions this month. So stronger-than-usual cash flow combined with free trades means that I spread capital around a lot more than I usually would have.

Early in the month, I picked up an additional 31 shares of Verizon Communications Inc. (VZ) at $42.72 per share. I’m not a huge fan of the telecommunications industry, but I think the valuation and yield make sense down in the low $40s.

I also snagged an additional 5 shares of International Business Machines Corp. (IBM) at $140.61 after a rough quarter sent the stock cratering. The yield is outstanding, the payout ratio remains very low, and the dividend will likely continue to grow at a very robust rate. The company doesn’t really need to grow at all from here for it to provide everything I need. But at some point, the revenue will need to stabilize.

Another stock that’s been suffering as of late, National Oilwell Varco, Inc. (NOV), remains very appealing to me. The long-term picture remains bright, but the exact time to buy stock in high-quality companies is when they’re absolutely beat down. Well, that’s what you have here. I picked up an additional 25 shares at $38.63 and another 5 shares at $36.21 after reducing my stake via a tax-loss harvesting last month.

Apple Inc. (AAPL), the largest publicly traded company in the world by market cap, has seen its stock decline even while results remain as strong as ever. So I averaged down on my position with another 5 shares at $110.19.

Notice a theme? Well, it continues. I also added my position in Wal-Mart Stores, Inc. (WMT). I’m topped up here, but found room for another 5 shares at $60.36. I don’t anticipate buying any more WMT, but I think the stock is meaningfully cheap right now. They certainly face real challenges, but the stock is down more than 30% on the year. While it was overvalued at the start of the year, that’s far more volatility than what the stock saw during the financial crisis, which is pretty amazing when you think about it.

I also bought more stock in Armanino Foods of Distinction Inc. (AMNF), which is just this wonderful little food company out of California. Results continue to impress, although I have to keep in mind that the company is really tiny (the market cap is just a little north of $60 million). So I have to appropriately manage that risk. But I grabbed just 50 shares at $1.94.

The healthcare REITs remain, in my view, really cheap here considering the long-term demographic tailwinds. So I added to my HCP, Inc. (HCP) position three times in October – 20 shares at $38.29, 10 shares at $38.77, and 10 shares at $37.32. And since this update is coming a few days into November, I also had an opportunity already this month to add once more (and likely for the last time), picking up 15 shares at $36.62.

However, I was also busy adding new positions to the Fund. Just like with the positions I added to, I remained focused on dividend growth stocks that present value, quality fundamentals, competitive advantages, and bright future prospects. I’m also mindful ofsector allocation and industry exposure. Of course, this has been my modus operandi since I started investing back in early 2010.

I initiated a stake in Potash Corporation of Saskatchewan (POT) very early in the month by grabbing 50 shares at $21.35. I then added to that position twice – 15 shares at $22.00 and 5 shares at $20.64. The stock has been hammered by dual concerns regarding potash pricing weakness and the potentially pricey takeover of rival K+S Potash, but the latter concern has now evaporated after the offer was withdrawn. The stock hasn’t recovered yet, but the current yield, at 6.93%, is approximately three times the five-year average. Meanwhile, every other basic valuation metric is substantially lower than its recent historical average. The stock appears significantly undervalued to me. And I’m excited to now be in the fertilizer business, which itself has long-term demographic tailwinds.

An interesting company, Computer Programs & Systems, Inc. (CPSI), recently popped up on my radar, and after taking a really good look at the company, I initiated a stake with 25 shares at $43.94. I don’t regret the logic, but the timing could have been better. After a fairly rough quarter, the stock dropped precipitously (much of which was warranted). I averaged down heavily with another 15 shares at $36.74. The fundamentals here are absolutely outstanding, but they’re making some changes whereby they focus less on system sales and more on service (that should provide recurring revenue). This, in my view, is short-term pain for long-term gain, but I’m going to watch this stock a bit more carefully than most. Nonetheless, the profitability is otherworldly, they have no debt, and the business (providing hospitals with necessary electronic records systems and administrative services) is fascinating in the aspect that demand should remain strong for years to come.

As discussed recently, I initiated a stake in Houston-based CenterPoint Energy, Inc. (CNP)with 65 shares at $18.62. I added another 15 shares at $18.56.

I noted last month that I planned on once more initiating a stake in BHP Billiton PLC (BBL)after selling out of my stake for tax-loss harvesting purposes. Well, I did just that. A new position in the world’s largest miner was initiated with 45 shares at $34.95. I purchased 5 more shares at $32.16. I don’t anticipate making this position as large as it was before due to the fact that it was larger than I wanted it to be, but I’m pretty comfortable here with 50 shares. It’s a highly cyclical business and FCF is basically just covering the dividend, so it’ll be interesting to see what the next two or three years look like for the firm.

Retail is one of my least favorite industries, so it’s surprising that I was pretty active there this month. I added to my WMT stake, as mentioned above. But I also initiated a position in Whole Foods Market, Inc. (WFM). The stock is down almost 40% YTD, which seems disconnected from underlying results. Meanwhile, it’s a premium brand with an extremely loyal and enthusiastic customer base. I picked up 20 shares at $32.82 and another 5 shares at $30.03. The yield leaves a lot to be desired, but the stock is as cheap as I’ve ever seen it. I plan on keeping this position small, however.

Another retail play (albeit apparel), I initiated a stake in Gap Inc. (GPS) with 25 shares at $27.00. Two out of their three global brands remain challenged, but Old Navy is killing it. I have an Old Navy within walking distance to my apartment, and I have to say it’s consistently busy. The apparel also appears particularly high quality for the price. I was in need of some clothes myself, so I took that opportunity to help contribute to my own bottom line by picking up a few pieces. The margins are surprisingly high to me because I bought seven different pieces of apparel and spent less than $40. Morningstar has this stock about 60% undervalued, and I initiated a position after coming to a similar conclusion myself. I’m excited to see what this position looks like in five or so years.

Noticeably, a number of stocks were unusually volatile this month. One was Yum! Brands, Inc. (YUM). It’s long been on my watch list, but the valuation has kept me from buying. However, after a ~20% drop on challenging earnings, I finally initiated a stake with 10 shares at $67.42. I didn’t think the stock was all that cheap even after the big drop, but it’s since rebounded rather strongly.

A similar story played out for VF Corp. (VFC). Great business, but the stock always seemed to reflect that (and then some). But a one-day double-digit drop in the stock brought it into a range that I thought was fairly reasonable. Again, not particularly cheap, but good enough to initiate a stake and see where it goes. I bought 10 shares at $65.25. It, too, has rebounded a bit since then. This one isn’t a household name, but their fundamentals and brands are outstanding. I wish I would have bought years ago, to be honest.

I mentioned at the end of last year that there were a few themes I was paying attention to as it relates to the portfolio and its industry exposure, long-term health, and income growth. One theme is e-commerce and how that positively affects volumes for major shippers like United Parcel Service, Inc. (UPS). The stock isn’t very cheap right now; it seems roughly fairly valued. But I think now is as good a time as any to initiate a stake in the world’s largest shipper. With the way e-commerce continues to grow, I can’t imagine they won’t be making a lot more money and sending out much bigger dividends a decade from now. I purchased 10 shares at $102.85. I’m actively interested in buying more. But a cheaper price would be even better.

Perhaps the most expensive stock I bought in October, I finally initiated a stake inStarbucks Corporation (SBUX) with 10 shares at $62.76. It’s not cheap. In fact, I think it’s at the upper end of fair value, but I’m also not sure one needs a big margin of safety here on Starbucks. I initiated a stake after the quarterly report came out, which was absolutely fantastic. They also announced a 25% dividend increase. The yield isn’t as high as I’d like, but I think the business is one of the best in the entire world. I’ll at least feel better about buying coffee when I spend my 4-5 hours per day over there writing and drinking away.

This is another stock I regret not buying years ago. The valuation kept me on the sidelines, but I now see I should have just paid up. It’s funny, but I often hear about how you shouldn’t commit capital to your “50th idea”, yet Starbucks was my 80th idea. Just so many wonderful businesses out there. Doesn’t mean The Coca-Cola Co. (KO), Union Pacific Corporation (UNP), Johnson & Johnson (JNJ), or any of the other 79 stocks that preceded this pick are any less worthy of my capital over the long haul. It’s just a situation where there is more than 20 or 30 really high-quality dividend growth stocks for the long term that an investor can buy.

As noted earlier, I’m active already in November. This update is coming a few days into November, so it’s encompassing purchases across the month of October as well as capital I’ve deployed since November started.

I also noted earlier that I think the healthcare REITs are providing huge opportunities here when looking at the growth, value, yield, demographic tailwinds, and long-term prospects. So I initiated a stake in likely the last healthcare REIT that I’ll own a slice of, buying 20 shares of Ventas, Inc. (VTR) at $53.54.

Lastly, 82 stocks into the portfolio and I finally invested in a business development company. I’m not overwhelmingly enthusiastic about BDCs in general because you quite frankly don’t know exactly what you’re buying into. I view the risk-reward relationship as pretty aggressive. You basically have to trust that management is going to make the right investments. That said, it’s an exciting business model in the sense that you’re gaining exposure to a lot of smaller companies that you ordinarily wouldn’t have access to.

I initiated a position in Main Street Capital Corporation (MAIN) after purchasing 40 shares at $30.28. Of all the BDCs I looked at, this one appears to be the most well run. Theirportfolio is incredibly diversified, and their track record for net income growth, NAV growth, and dividend growth since their IPO is really impressive. The stock yields over 7% here with a monthly dividend and the five-year dividend growth rate is just under 6%. Moreover, they pay semi-annual special dividends that tend to be sizable. This is a speculative investment, but I think it’s the least speculative BDC out there. And my portfolio has the room for the speculation, especially considering the blue-chip base my Freedom Fund is built upon.

All of this activity made a huge impact on my annual dividend income. Adding it all up, my annual dividend income increased by $962.76. I couldn’t be more thrilled with that kind of boost. November and December will likely be nowhere near as effective in this regard, but I’ll be happy if I can add just another $500 to my annual dividend income before the year ends.

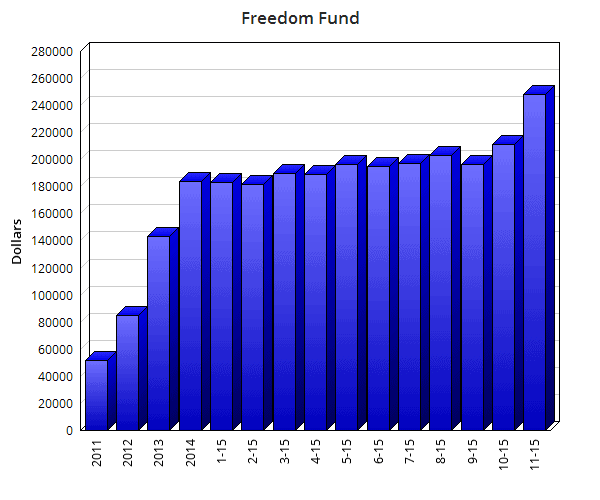

The current market value of the Freedom Fund stands at $248,261.56, which is a 17.4%increase since last month’s published value of $211,444.20.

The S&P 500’s record-breaking October run (the monthly increase in terms of points was the highest ever) certainly didn’t hurt the positive change in value, but I would have rather seen the portfolio drop in value so that my capital could go that much further. Didn’t turn out that way. In fact, this was the largest increase in portfolio value from one month to another that I’ve ever experienced. I expect that’s a record that will naturally be broken at some point within the next year or two as the portfolio’s value increases, which means percentage changes will impact it that much more.

The Fund continues to move in the right direction, all in all. Warren Buffett has compared Berkshire’s collection of businesses to a “masterpiece”, and I look at my own portfolio inmuch the same way. I’m painting my own version of a masterpiece with this really fantastic collection of world-class businesses that should send me increasing dividends for decades to come. It’s coming together so nicely. I really couldn’t be prouder of this collection considering that I started out with absolutely nothing (no money, no stocks, no prior investment knowledge) less than six years ago.

As always, thank you for all your continued support. I can only hope that you find value, inspiration, and motivation in these updates. If I can do it, so can you. I truly believe that financial independence is out there waiting for almost all of us.

The Fund now has positions in 82 different companies. This is an increase since last month since I initiated stakes in 12 new businesses. I expect the rate at which I open new positions to slow dramatically over the near future as I whittle my watch list down.

These updates are mainly designed to show the increase or decrease in the value of the underlying equities I’m invested in, but the main purpose of investing in dividend growth stocks is to build a rising and sustainable stream of dividends over time. Thus, I don’t put too much emphasis on these monthly updates. I think it is a good idea, however, to keep track of the rising (or falling) value of one’s securities and be aware of where they are in terms of the marketplace and whether or not certain stocks are attractively priced. I find it a helpful exercise to update the values monthly. It gives me fresh perspective on which equities are performing well and which aren’t, and from there I can make educated decisions (based on further due diligence) on which stocks I’d like to add fresh capital to (while considering portfolio weight as well).

Full Disclosure: Long all aforementioned stocks.

How was your October? Stay as busy as you would have liked? Take advantage of any opportunities?

Thanks for reading.

This article was written by Dividend Mantra. If you enjoyed this article, please subscribe to my feed [RSS]

This article was written by Dividend Mantra. If you enjoyed this article, please subscribe to my feed [RSS]