Summary:

ALV had to suspend its dividend in 2009 due to the car industry crisis. Since then, the dividend payment has grown by 58% CAGR from 2010 to 2015.

The company benefits from various factors in an industry promoting more safety.

This is a cyclical and highly competitive industry. Pressures on margins are constant and the company won’t keep up with such aggressive dividend growth in the future.

DSR Quick Stats

Sector: Consumer Cyclical

5 Year Revenue Growth: 12.53%

5 Year EPS Growth: 35.05%

5 Year Dividend Growth: 58.79%

Current Dividend Yield: 1.82%

What Makes Autoliv (ALV) a Good Business?

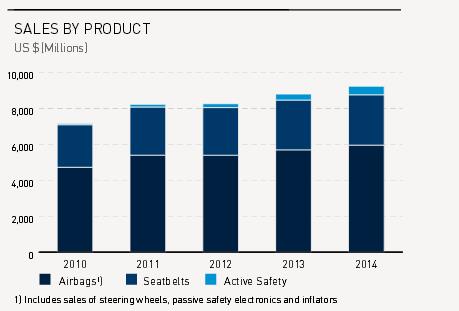

This is how Autoliv management described the company in their 2014 annual report. We can’t be against virtue, can we? More seriously, Autoliv is a designer and manufacturer of safety products for the automobile industry. Their product offering includes air bags, seatbelts, steering wheels, passive safety electronics and active safety systems such as radar, night vision and cameras. The company is incorporated in Delaware but its headquarters are based in Stockholm, Sweden.

Source: ALV 2014 annual report

Source: ALV 2014 annual report

They are among the leaders in the car safety industry. For example, ALV owns 7% of all automotive patents for its side-impact air bags. The company spends around 6% of its sales on research and development to stay ahead of their competition.

The overall perspectives are bullish for such businesses since there is an increasing interest in car safety. First, the rising New Car Assessment Program (NCAP) safety standards force car makers to allocate higher budgets for safety in their design. Second, rising income in emerging markets lends to more people interested in safety as opposed to luxury. As the car industry is currently doing well, all perspectives come are leading to a bright future for the upcoming years for ALV.

Ratios

Price to Earnings: 25.62

Price to Free Cash Flow: 58.78

Price to Book: 3.219

Return on Equity: 12.39%

Price to Free Cash Flow: 58.78

Price to Book: 3.219

Return on Equity: 12.39%

Revenue

Revenue Graph from Ycharts

Revenue Graph from Ycharts

As you can see, ALV is evolving in a highly cyclical market. 2008 car makers difficulty affected the company greatly showing an important dip in its revenue. Since then, as the industry has done much better, so has Autoliv.

How ALV fares vs My 7 Principles of Investing

We all have our methods for analyzing a company. Over the years of trading, I’ve been through several stock research methodologies from various sources. This is how I came up with my 7 investing principles of dividend investing. The first four principles are directly linked to company metrics. Let’s take a closer look at them.

Source: Ycharts

Source: Ycharts

Principle #1: High dividend yield doesn’t equal high returns

According to much financial research, high dividend yielding stocks have a bad reputation of giving investors nothing but their distribution. 2nd quartile dividend yield stocks usually provide better total returns as they have more room to make both their business and dividends grow. High yield stocks can be found in stagnating or mature industries where growth is difficult to generate.

Source: data from Ycharts.

Source: data from Ycharts.

The company doesn’t show a stellar dividend payment history. While the dividend yield is reasonable since the company “reset” its dividend policy back in 2010, the yield variation is definitely higher than most classic dividend growth stocks.

We keep repeating that past data is not a guarantee for future returns. In this case, if we “forget” about the 2008 crisis, the company currently meets the first principle.

Principle#2: If there is one metric, it’s called dividend growth

It is true the dividend payment dropped following the market crash. However, the company soon recovered what was lost and the dividend per share increases shown in the previous graph could show a steadily increasing line from 2006 to 2015 covering the gap between 2009 and 2012. I often consider 2008 as a statistical error as it never happened in the past and won’t likely happen again in the near future. The overall look of the company’s dividend growth perspective remains intact.

Principle #3: A dividend payment today is good, a dividend guaranteed for the next ten years is better

If dividend growth is the most important metric according to my investment analysis process, the company’s ability to maintain this growth over time is also very important.

Source: data from Ycharts.

Source: data from Ycharts.

The company maintains a more than appreciable payout ratio of 46% while the past 3 year’s dividend growth stands at 7% which is most likely to be the new pace for increases in the future.

Principle #4: The Foundation of a dividend growth stock lies in its business model

Metrics show that the company can keep up with a decent dividend growth rate for the years to come. ALV also modified its business model to improve its chances of growth in the future. The company now shows roughly 60% of its work force located in low-cost countries compared to only 30% back in 2002. ALV invests massively in research and development as safety improvements will come from new technology. The company has shown in the past its ability to present improved products with higher margins in order to keep its distance from its peers.

What Autoliv Does With its Cash?

As many other have in the past 5 years, the company used lots of its cash to buy back shares while increasing its dividend. With a 6% sales budget for research and development, management shows they want to not only compensate investors with dividends, but with future growth as well.

Investment Thesis

The idea of investing in Autoliv is to select a company that is in the right place at the right time with the car industry growing and the demand for additional safety. If car makers want to reach 4 and 5 star safety ratings, they will need Autoliv products to achieve their goal.

A look at their most recent quarters might tell you otherwise at first glance:

However, you have to dig deeper to fully understand what happened from 2014 to 2015. As you know already, currency headwinds have been the most discussed topics among many international companies. ALV is no exception. In fact, organic sales grew by 8% and EPS grew by 24% considering currency neutral numbers.

The company has seen double digit growth in many countries such as Europe, Japan and the rest of Asia. The company expects to post 9% organic growth sales for the last quarter of the year. The investment thesis is being validated by this statement.

Risks

While the interest for additional safety in cars is undeniable, ALV’s other growth factor is not too strong. In fact, the company is also dependent on emerging markets where the demand for safer cars is increasing. With China’s economy experiencing reduced growth, ALV is facing, once again, its vulnerability to a highly cyclical market.

The other risk associated with this company is that ALV doesn’t have any incredible competitive advantage. It is true they invest massively in R&D and the benefit of a good reputation. However, the company continuously faces fierce competition where car makers request volume discounts and reduced prices for product agreements. So far, ALV has been able to control this risk by being on top of the technological advancements in their field.

Should You Buy ALV at this Value?

The last section of this analysis is dedicated to finding ALV’s intrinsic value. We start by looking at how the market has valued the company over the past 10 years:

Source: data from Ycharts.

Source: data from Ycharts.

At first glance, a PE ratio of 25 seems very high. The company hasn’t been trading with such a high multiplier over the past 10 years. I understand why there is a relative hype around the car industry, but I should remind investors that cyclical companies at the top of their cycle are always overpriced.

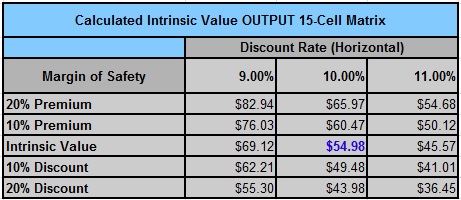

In order to have a better idea, I will use a double stage dividend discount model. Since the company evolves in a cyclical industry, I will use an 10% discount rate. The company is doing well, but there are several external risks that management has little control over. As far a dividend growth rate, I think the upcoming years will continue to follow the current uptrend. Therefore, I will use the past 3 years dividend growth rate of 7%. After the first 10 years, I will use a 5% dividend growth rate that will be more conservative.

Here again, the company looks highly overvalued. This is often the case when using a DDM with a low dividend yield. The market expects more than simply dividend growth when it looks at ALV.

Final Thoughts on ALV – Buy, Hold or Sell?

At the moment, I think ALV is more in the “hold” level than a buy. The company shows strong potential in the upcoming years but it is not trading at discount at the moment. It is definitely overvalued. In the meantime, investors will benefit from a good dividend growth rate even though the yield is not spectacular.

Disclaimer: I hold ALV in my DividendStocksRock portfolios.This article was written by Dividend Monk. If you enjoyed this article, please subscribe to my feed [RSS]