One of the reasons many market observers believe this recession will be a long one is the growth in consumer debt over the years. As consumers now focus on paying down debt levels, they won't be able to spend to the same extent; thus, fewer goods will be produced, acting as a drag on GDP. But what is worth mentioning is that this argument is used in every recession by those who anticipate a depression, so are things really that different this time?

In an article in Forbes magazine in 1991, Ken Fisher responded to those who argued that the recession of the early 1990s was to turn into a depression because mountains of consumer debt had to be paid back before the economy could once again grow. In Fisher's view, this argument was nothing more than fear mongering, as it ignored consumer income. While absolute debt levels were high, debt as a percentage of income was not.

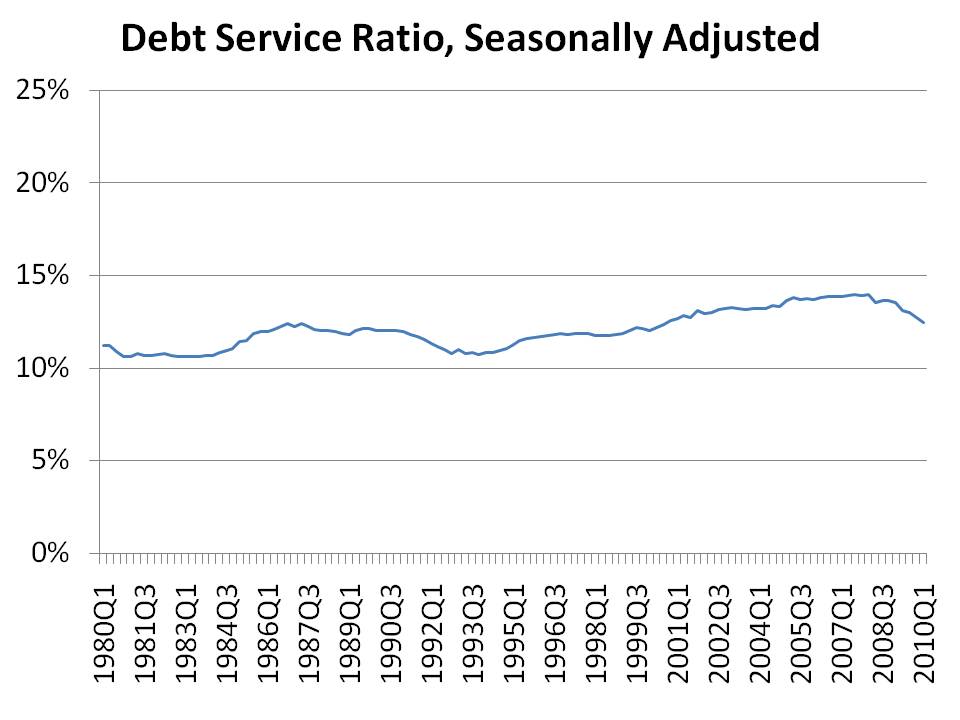

Today, we hear similar arguments about consumer debt levels. But as debt has risen over the years, so has productivity (thanks to education, innovation and investment). So let's consider these debt levels in relation to income. The following chart illustrates the consumer household debt service ratio (DSR), which is the ratio of required mortgage and consumer debt to disposable personal income:

The DSR is clearly not out of line with what it has been over the last 3 decades. Though it is still higher now than it was in the early 1980s and early 1990s, how is one to know what is the "right" level of consumer debt? Fisher argued that as long as there are assets that generate substantially more returns than the cost of debt, there will be people who exploit such opportunities, thus driving up the level of debt.

Whether the DSR will turn upward soon, or continue downward for some time is anybody's guess. The point is, debt levels are not way out of line with what they have been in the past, and that the ideal consumer debt level for this economy may well be higher than debt levels stand right now.

Reading articles from previous recessions can offer investors perspective. Often, the same situations are seen again and again, but are claimed to be "different this time". Educating oneself is the best defense against spurious arguments. However, timing when debt levels will start to once again expand is very difficult to do. As such, investors are better off keeping perspective with respect to the market, and putting their energy towards investing in companies trading at discounts to their intrinsic values.

Source: Federal Reserve

This article was written by Saj Karsan of Barel Karsan. If you enjoyed this article, please consider subscribing to my feed.

17 hours ago